Europe sugar substitute Market Research Report – Segmentation by Product Type (High-Intensity Sweeteners and Low-Intensity Sweeteners); By Source (Plant-based and Synthetic); By Application (Food and Beverages, Pharmaceuticals and Healthcare, and Personal Care and Cosmetics); and Region; - Size, Share, Growth Analysis | Forecast (2024– 2030)

Europe Sugar Substitutes Market Size (2024-2030)

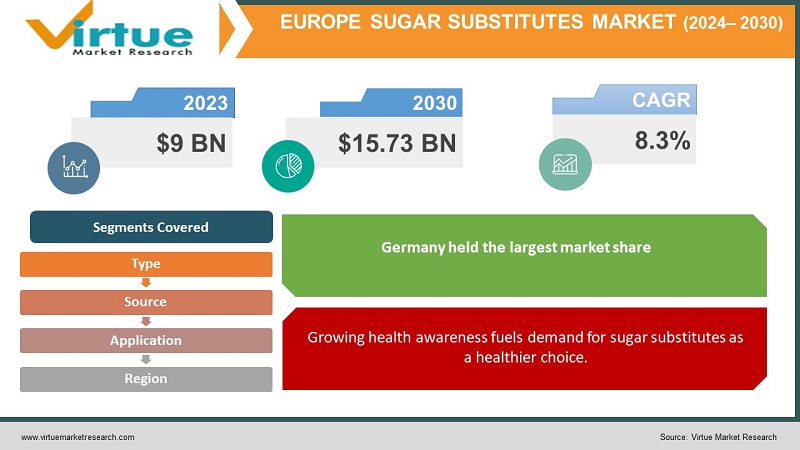

The European sugar substitute market was valued at USD 9 billion in 2023 and is projected to reach a market size of USD 15.73 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to grow at a CAGR of 8.3%.

The European sugar substitute market is driven by a growing awareness of the health benefits of reduced sugar intake, particularly for weight management and blood sugar control. This awareness, coupled with the rising prevalence of chronic diseases like obesity and diabetes, is fueling the demand for sugar substitutes. Consumers are increasingly seeking low-calorie and sugar-free food and beverage options, further propelling market growth. Rising disposable incomes allow for more spending on premium and functional products, while a trend toward natural ingredients is driving the popularity of stevia and erythritol over artificial sweeteners.

Key Market Insights:

The European sugar substitute market is on a steady rise, fueled by a growing health consciousness among consumers. As individuals become more aware of the benefits of reduced sugar intake, particularly for weight management and blood sugar control, the demand for sugar substitutes naturally increases. This trend is further amplified by the rising prevalence of chronic diseases like obesity and diabetes in Europe. This health focus is coupled with a shift in consumer preferences towards low-calorie and sugar-free options. As disposable incomes increase, consumers are willing to spend more on premium and functional products. This has led to a growing preference for natural sweeteners like stevia and erythritol, perceived as healthier alternatives to artificial sweeteners. The market extends beyond just food and beverages, finding applications in diverse sectors like pharmaceuticals, healthcare, personal care, and even cosmetics. Looking ahead, continued innovation in the development of new and improved sugar substitutes with better taste profiles and functionalities is expected to further drive market growth. This focus on innovation ensures that the industry remains competitive and caters to the evolving preferences of health-conscious consumers.

Europe Sugar Substitutes Market Drivers:

Growing health awareness fuels demand for sugar substitutes as a healthier choice.

A key driver of the European sugar substitute market is the increasing emphasis on health and wellness among consumers. People are becoming more informed about the negative impacts of excessive sugar consumption, including weight gain, difficulties with blood sugar control, and potential links to other chronic diseases. This awareness fuels demand for sugar substitutes, which are perceived as a healthier alternative to managing sugar intake.

Rising chronic diseases in Europe create a need for sugar substitutes as a management tool.

Another significant driver is the growing burden of chronic diseases in Europe, particularly obesity and diabetes. These conditions are often linked to excessive sugar intake, making sugar substitutes a potential tool for managing them. As the prevalence of these diseases continues to rise, the demand for sugar substitutes is expected to climb alongside it.

Shifting consumer preferences towards low-calorie and sugar-free options drives market growth.

Consumer preferences are also playing a major role in driving the market. There's a clear trend towards low-calorie and sugar-free food and beverage options. This shift reflects a desire for healthier lifestyles and a growing focus on preventive health measures. Sugar substitutes cater to this demand by offering a way to enjoy sweet-tasting products without the associated drawbacks of excessive sugar consumption.

Premiumization and natural ingredient trends boost the popularity of stevia and erythritol.

Rising disposable incomes are allowing European consumers to spend more on premium and functional food and beverage products. This trend, coupled with a preference for natural ingredients, is boosting the popularity of natural sweeteners like stevia and erythritol. These substitutes are perceived as healthier alternatives to traditional artificial sweeteners, further driving market growth within the natural segment.

Diverse applications and constant innovation propel market expansion and cater to evolving preferences.

The European sugar substitute market extends beyond just food and beverages. Sugar substitutes find applications in various sectors, including pharmaceuticals, healthcare, personal care, and even cosmetics. This broadens the market reach and opens doors for further growth. Additionally, continuous innovation in developing new and improved sugar substitutes with better taste profiles and functionalities is expected to further drive market expansion. This focus on innovation ensures the industry remains competitive and adapts to evolving consumer preferences for healthier and more functional products.

European Sugar Substitutes Market Restraints and Challenges:

Despite the promising growth drivers, the European sugar substitute market faces some hurdles. Stringent regulations regarding safety, labeling, and approval processes, particularly for artificial sweeteners, can hinder market expansion. These regulations, coupled with varying standards across European countries, can complicate product development and market entry for manufacturers. Additionally, some consumers remain hesitant due to a negative perception of artificial sweeteners, often fueled by ongoing scientific debates and inconclusive studies regarding their potential health risks. Market affordability can also be impacted by fluctuating raw material costs, potentially limiting consumer choices. Furthermore, the continued presence of readily available and affordable natural sugar, alongside efforts to promote its sustainable production, poses a competitive challenge to sugar substitutes. Finally, the market grapples with the ongoing challenge of developing substitutes that perfectly replicate the taste and functionality of sugar, which can limit their adoption in specific applications and hinder wider consumer acceptance. Overcoming these restraints and challenges will be crucial for the European sugar substitute market to reach its full potential.

European Sugar Substitutes Market Opportunities:

The European sugar substitute market holds exciting opportunities for future growth and innovation. The rising demand for natural ingredients creates fertile ground for the expansion of the natural sweetener segment, with stevia, erythritol, and other plant-based options gaining traction as healthier alternatives. Furthermore, continuous research and development can lead to improved taste profiles that closely mimic sugar, overcoming a key challenge and potentially broadening their appeal. Additionally, exploring and highlighting the potential functional benefits of certain sugar substitutes, such as prebiotic effects or blood sugar control support, can unlock new market opportunities. Targeted marketing and educational initiatives are crucial to addressing consumer concerns and misconceptions surrounding sugar substitutes and promoting their potential health benefits and safety. Moreover, exploring new applications beyond traditional food and beverage sectors, such as nutraceuticals, dietary supplements, and even pet food, can offer significant growth potential. Finally, aligning with sustainability principles through ethical sourcing and eco-friendly packaging can attract environmentally conscious consumers and enhance brand image, further propelling the market forward. By capitalizing on these opportunities, stakeholders can ensure the European sugar substitute market thrives in the coming years.

EUROP SUGAR SUBSTITUTES MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2023 - 2030

Base Year

2023

Forecast Period

2024 - 2030

CAGR

8.3%

Segments Covered

By Product Type, Source, application, and Region

Various Analyses Covered

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

Italy, Spain, Russia, Germany, UK, France, Rest of Europe

Europe Sugar Substitutes Market Segmentation: ByType:

High-Intensity Sweeteners

Low-Intensity Sweeteners

The largest and fastest-growing segment in the European sugar substitute market by type is high-intensity sweeteners, driven by the increasing consumer preference for natural ingredients. Fewer sweeteners are needed to provide the same sweetness as high-intensity sweeteners since they are substantially sweeter than table sugar (sucrose). The increasing worldwide trend towards health and well-being is anticipated to expand the range of applications for high-intensity sweetness.

Europe Sugar Substitutes Market Segmentation: BySource:

Plant-based

Synthetic

The synthetic segment is the largest. Aspartame, saccharin, and sucralose are examples of artificial sugar replacements that have traditionally been widely utilized in the food and beverage business. These artificial sweeteners provide sweetness without the calorie count of sugar and are frequently used in a range of tabletop sweeteners, drinks, and processed foods. Because they are so widely used by both food makers and consumers, synthetic sugar replacements continue to have a considerable market share in Europe, despite concerns over potential health impacts and artificiality. The plant-based segment is the fastest-growing, driven by consumer preference for natural ingredients. Rising health consciousness has been extremely beneficial for this category. This segment encompasses natural sweeteners like stevia and erythritol.

Europe Sugar Substitutes Market Segmentation: ByApplication:

Food and Beverages

Pharmaceuticals and Healthcare

Personal Care and Cosmetics

The European sugar substitute market is segmented by application, with food and beverages being the dominant segment due to their widespread use in various low-calorie and sugar-free products. However, the pharmaceuticals and healthcare segment is expected to see the fastest growth in the coming years due to the increasing demand for sugar-free medications and diabetic supplements.

Europe Sugar Substitutes Market Segmentation: Regional Analysis:

UK

Germany

France

Italy

Spain

Rest of Europe

Germany is the largest growing market, driven by a diverse food and beverage industry and a strong emphasis on product innovation. German consumers are increasingly health-conscious and receptive to sugar substitutes. However, price sensitivity remains a factor, and affordability plays a crucial role in consumer choices. The market sees a balanced presence of both natural and artificial sweeteners, with ongoing innovation focusing on improved taste profiles and functionality. The UK market for sugar substitutes is the fastest-growing, driven by a growing health-conscious population and increasing awareness of the benefits of reduced sugar intake. Consumers are actively seeking low-calorie and sugar-free options, particularly in beverages and baked goods. The market also sees a growing preference for natural sweeteners like stevia and erythritol. Regulatory factors play a significant role, with the UK aligning with broader European Union regulations regarding sweetener safety and labeling. The French market for sugar substitutes is characterized by a growing demand for natural sweeteners, particularly stevia, which aligns well with the French preference for natural and high-quality ingredients. Regulatory scrutiny in France is relatively moderate compared to other European countries, but safety and labeling requirements still play a crucial role. The market caters to a diverse range of applications, including food and beverages, pharmaceuticals, and personal care. The Italian sugar substitute market is experiencing moderate growth, influenced by both health-conscious consumers and a strong cultural preference for traditional desserts and beverages. While there is a growing awareness of the benefits of reduced sugar intake, the market still sees a significant presence of traditional sugar-based products. The adoption of natural sweeteners is gaining traction, but artificial sweeteners remain prevalent, particularly in specific product categories. The Spanish market for sugar substitutes is expected to see significant growth in the coming years, driven by rising disposable incomes and increasing health awareness among consumers. The market sees a growing preference for natural sweeteners, alongside a continued presence of artificial sweeteners. Affordability is a key factor influencing consumer choices, and price sensitivity plays a crucial role in market dynamics. Continued innovation and education regarding the benefits of sugar substitutes are expected to further drive market growth in Spain.The rest of the Europe segment encompasses various smaller European countries with diverse market dynamics. Eastern European countries, in particular, are expected to see significant growth in the sugar substitute market due to rising disposable incomes, increasing awareness of health benefits, and growing adoption of Western European dietary trends. However, regulatory environments and consumer preferences can vary significantly across these countries, requiring a nuanced approach from market players.

COVID-19 Impact Analysis on theEuropean Sugar Substitutes Market:

The COVID-19 pandemic has had a dual impact on the European sugar substitute market. Initial disruptions included supply chain issues due to lockdowns, leading to temporary shortages and price fluctuations. Additionally, shifting consumer behavior during the early stages, with a focus on stockpiling essentials, might have caused a dip in demand. Production slowdowns due to safety measures also played a role in temporary availability issues. However, the long-term outlook appears positive. The pandemic has heightened awareness of health and well-being, potentially leading to a sustained rise in demand for healthier options like sugar substitutes. The growth of e-commerce platforms, which boomed during the pandemic, could further benefit sugar substitute sales as consumers shift to online grocery shopping. Additionally, the growing interest in immune-boosting products might create opportunities for sugar substitutes marketed with potential benefits like weight management, which can indirectly support immune health. Overall, while the initial stages of the pandemic caused some disruption, the long-term impact on the European sugar substitute market is expected to be positive. The growing focus on health and immunity, coupled with the rise of e-commerce and potential benefits linked to weight management, could contribute to market growth in the coming years. Despite these considerations, the market is expected to adapt and emerge stronger due to underlying growth drivers and a potential shift towards a more health-conscious consumer landscape in the post-pandemic era. Overall, while the initial COVID-19 impact might have been negative, the long-term outlook seems mixed. The food service sector's recovery might be slow, but opportunities exist in the rising home cooking trend, e-commerce adoption, and a potential shift towards healthier options. Manufacturers who adapt their products and strategies to cater to these evolving preferences are well-positioned to thrive in the post-pandemic European jams and preserves market.

Latest Trends/ Developments:

The European sugar substitute market is buzzing with exciting developments. The demand for natural sweeteners like stevia and erythritol is on the rise, prompting manufacturers to create innovative blends that deliver the desired sweetness and functionality. Furthermore, research is focused on improving taste profiles to closely resemble sugar, addressing a key consumer concern. Additionally, sustainability is becoming paramount, with companies emphasizing ethically sourced materials, eco-friendly packaging, and reduced environmental impact. The market is also witnessing expansion beyond food and beverages, with sugar substitutes finding applications in nutraceuticals, dietary supplements, and even pet food. Targeted marketing and educational initiatives are crucial to address consumer concerns and promote the potential health benefits and safety of sugar substitutes, particularly for artificial options facing lingering negativity. Regulatory bodies are constantly updating safety and labeling requirements, requiring manufacturers to stay informed and compliant. Finally, an increase in mergers and acquisitions indicates a dynamic market where companies are seeking to expand their reach, strengthen positions, and acquire new technologies. By staying abreast of these trends, stakeholders can position themselves to capitalize on opportunities and contribute to the continued growth and evolution of the European sugar substitute market.

Key Players:

Cargill

Ingredion

Archer Daniels Midland

Tate & Lyle

Süsswarenfabrik J.D. Sprengel

Ajinomoto

Roquette Frères

PureCircle

JK Sucralose

MacAndrews & Forbes

To Learn more about this report,

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. Europe Sugar substitute Market– Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. Europe Sugar substitute – Executive Summary

Fill out the form below and our team will get back to you shortly

FAQ's

The European sugar substitute market was valued at USD 9 billion in 2023 and is projected to reach a market size of USD 15.73 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to grow at a CAGR of 8.3%.

Growing focus on health and wellness, rising prevalence of chronic diseases, shifting consumer preferences, premiumization, demand for natural ingredients, diverse applications, and innovation focus are the main market drivers

Based on application, the market is divided into food and beverages, pharmaceuticals and healthcare, personal care and cosmetics

. The most dominant region in the European sugar substitute market is Germany, driven by its diverse food and beverage industry, strong emphasis on innovation, and growing health-conscious population

Cargill, Ingredion, Archer Daniels Midland, Tate & Lyle, Süsswarenfabrik J.D. Sprengel, Ajinomoto, Roquette Frères, PureCircle, JK Sucralose, and MacAndrews & Forbes are the major players.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-18738 | Published Date: October 2025 | Format: Excel and PDF

The Middle East and Africa Cold Cuts Market was valued at USD 35.93 billion in 2024 and is projected to reach a market size of USD 110.55 billion by the end of 2030. Over the forecast period of 2025-2030, the market is p...

Report Code: VMR-18663 | Published Date: October 2024 | Format: Excel and PDF

The Arabica Sourced Bioactive Compounds in Coffee Market was valued at USD 340 Million in 2024 and is projected to reach a market size of USD 513 Million by the end of 2030.

Report Code: VMR-15690 | Published Date: August 2023 | Format: Excel and PDF

The Global Online Ready-to-Drink Cocktails Market was valued at USD 8.2 billion in 2024 and will grow at a CAGR of 12% from 2025 to 2030. The market is expected to reach USD 16.2 billion by 2030.

Report Code: VMR-2118 | Published Date: July 2024 | Format: Excel and PDF

The Global Beauty Drinks Market was valued at USD 2.2 billion in 2024 and will grow at a CAGR of 14% from 2025 to 2030. The market is expected to reach USD 4.8 billion by 2030.

Report Code: VMR-1283 | Published Date: March 2024 | Format: Excel and PDF

The global chocolate powdered drinks market was valued at USD 2.92 billion and is projected to reach a market size of USD 5.28 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”