Family Entertainment Centers Market

The Family Entertainment Centers Market was valued at USD 34.45 billion in 2023. Over the forecast period of 2024-2030 it is projected to reach USD 73.81 billion by 2030, growing at a CAGR of 11.5%.

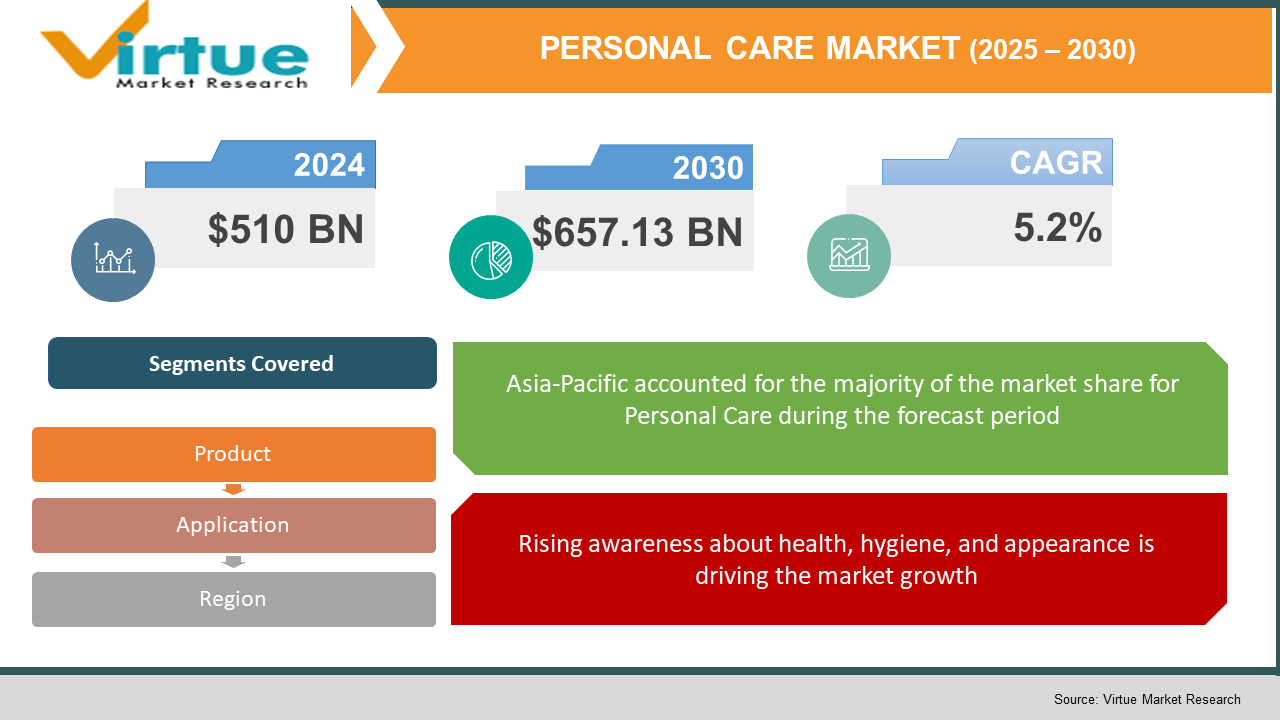

Explore reportThe Global Personal Care Market was valued at USD 510 billion in 2024 and will grow at a CAGR of 5.2% from 2025 to 2030. The market is expected to reach USD 657.13 billion by 2030.

The Personal Care Market includes a wide array of products aimed at maintaining personal hygiene, grooming, and health. These products encompass skincare, haircare, oral care, cosmetics, fragrances, and hygiene products such as deodorants, soaps, and sanitary items. With rising consumer awareness, the personal care market has evolved from basic hygiene to include luxury, wellness, and eco-conscious elements. Consumers today are more informed and selective, opting for personalized, ingredient-transparent, and sustainable products. The market’s expansion is being driven by urbanization, increased disposable incomes, social media influence, and the convergence of beauty and wellness. Emerging trends such as clean beauty, gender-neutral formulations, and digital beauty tools continue to redefine how consumers engage with personal care brands globally.

Key market insights:

Asia-Pacific accounted for 36% of the global personal care market share in 2024, making it the largest regional market.

Skincare remained the leading segment in 2024, contributing over USD 180 billion globally, driven by anti-aging and sun protection products.

E-commerce channels saw a 14% increase in personal care product sales year-on-year, primarily due to Gen Z and millennial consumers.

Demand for natural and organic personal care products grew by 17% in 2024, led by the US, Germany, and South Korea.

Men’s grooming products registered a CAGR of 6.8% from 2022 to 2024, as brands launched specialized skincare and haircare lines for men.

Personal care companies are increasingly investing in refillable and recyclable packaging, with sustainable packaging adoption growing by 11% in 2024.

Influencer and celebrity collaborations accounted for 21% of new brand launches globally in 2024, boosting brand recognition and reach.

Global Personal Care Market Drivers

Rising awareness about health, hygiene, and appearance is driving the market growth

One of the most significant drivers of the personal care market is the increasing consumer awareness regarding health, hygiene, and personal appearance. Today’s consumers recognize the strong link between appearance and self-confidence, as well as the social and professional implications of personal grooming. The COVID-19 pandemic intensified focus on hygiene, driving demand for hand sanitizers, antibacterial soaps, and hygiene-focused skincare. As education and access to information improve globally, even rural and semi-urban populations are adopting personal care routines. Awareness campaigns led by governments and NGOs also contribute to better hygiene practices, especially in developing countries. Additionally, the rise in screen time and video interactions through social platforms and professional meetings has led consumers to pay greater attention to their appearance, boosting categories like skincare, makeup, and haircare. This increased awareness has not only expanded product usage across age and gender groups but also deepened frequency of purchase and category diversification. Brands are leveraging this trend by offering products tailored for specific needs such as anti-aging, acne control, or skin brightening, along with educational content that helps consumers build personalized routines. This shift from basic hygiene to overall wellness and appearance is a long-term growth driver for the market.

Boom in e-commerce and digital engagement is driving the market growth

The rapid digitization of commerce and the rise of social media platforms have significantly transformed how consumers discover, evaluate, and purchase personal care products. E-commerce platforms offer convenience, access to international brands, personalized recommendations, and frequent promotional offers, all of which have attracted consumers globally. The boom in beauty-focused content on platforms like Instagram, TikTok, and YouTube has enabled even smaller brands to gain visibility and build loyal communities. Influencers and beauty vloggers play a key role in educating consumers, demonstrating products, and sharing honest reviews, which in turn fosters trust and drives purchase decisions. Artificial Intelligence and Augmented Reality technologies have further elevated the online shopping experience, enabling features like virtual try-ons and skin diagnostic tools that were once limited to physical stores. Direct-to-consumer (D2C) brands are thriving under this model, bypassing traditional retail channels and focusing on customer engagement, fast delivery, and product customization. As mobile and internet penetration increases, particularly in emerging economies, digital platforms are expected to become the dominant sales channel for personal care products. This digital transformation not only expands market reach but also provides valuable consumer insights, allowing brands to innovate and iterate faster than ever before.

Shifting preferences towards clean, natural, and sustainable products is driving the market growth

Environmental consciousness and concern for health have prompted a major shift in consumer preferences toward clean, natural, and sustainable personal care products. Clean beauty, characterized by formulations free of parabens, sulfates, and harmful chemicals, is becoming a mainstream expectation rather than a niche demand. Consumers are increasingly scrutinizing ingredient lists and favor brands that are transparent about sourcing, production processes, and ethical practices. Products with plant-based, cruelty-free, and vegan certifications are gaining traction, especially among younger consumers and urban populations. Additionally, sustainable packaging—such as biodegradable containers, refillable systems, and recyclable materials—is becoming a critical factor influencing buying decisions. Brands that fail to adopt eco-friendly practices risk losing relevance in the eyes of environmentally conscious consumers. Many companies are also adopting circular economy principles, where used packaging is collected and reused or responsibly disposed of. This demand is further supported by regulatory frameworks in Europe and North America that encourage green practices. Clean and sustainable personal care is no longer limited to premium segments; mass-market brands are also entering the space, making it more accessible. As this trend matures, it is likely to drive long-term structural changes in formulation, sourcing, and brand positioning.

Global Personal Care Market Challenges and Restraints

Complex regulatory compliance and formulation standards is restricting the market growth

One of the primary challenges in the personal care market is navigating the complex and evolving regulatory landscape. Each region has its own set of compliance requirements, ingredient restrictions, and labeling standards, making global expansion particularly challenging for brands. For example, the European Union has banned over 1,300 substances in cosmetics, while the U.S. Food and Drug Administration (FDA) regulates personal care under relatively looser frameworks. This disparity requires brands to create different product formulations for different markets, increasing R&D costs and complicating manufacturing processes. Furthermore, the growing demand for clean beauty has led to greater consumer scrutiny and legal expectations around “natural” or “organic” labeling, which are not uniformly defined across markets. Mislabeling or failure to meet transparency standards can result in reputational damage, product recalls, or litigation. In addition, companies must comply with regulations related to animal testing, which are prohibited in several countries, further complicating product development pipelines. The increased use of biotechnology and novel ingredients adds another layer of complexity, as these innovations often fall into regulatory gray zones. Overall, maintaining compliance across jurisdictions while innovating responsibly is a significant challenge that can limit the speed and scope of global market expansion.

Intense competition and price sensitivity in mass-market segments is restricting the market growth

While the personal care industry continues to grow, it is also becoming increasingly crowded and competitive, especially in mass-market segments. Large multinational corporations dominate shelf space and digital presence, but the rise of local players, private labels, and D2C startups is creating price wars and promotional saturation. These new entrants often rely on aggressive pricing strategies and unique selling propositions such as “clean,” “sustainable,” or “customized,” which appeal strongly to digital-native consumers. However, this abundance of choice can lead to brand fatigue and consumer indecision. Established brands face pressure to continually innovate and refresh their offerings while maintaining affordability and quality. Moreover, economic uncertainties and inflationary pressures have heightened price sensitivity among consumers, especially in emerging markets. As a result, buyers may opt for smaller sizes, multipurpose products, or budget-friendly alternatives. Profit margins are under strain, and brand loyalty is harder to sustain. For premium and luxury segments, there’s an added challenge of justifying value amidst increasing skepticism and economic scrutiny. The resulting market environment demands high agility, efficient cost management, and continuous brand differentiation. Without these, even well-established companies risk losing market share to more adaptive and price-competitive newcomers.

Market opportunities

The Global Personal Care Market offers a range of compelling growth opportunities driven by consumer shifts, technological advances, and regional diversification. One major opportunity lies in personalization. With the proliferation of AI and data analytics, brands can now offer highly personalized product recommendations, skincare regimens, and haircare formulations based on individual needs, preferences, and even genetic profiles. This level of customization builds trust and loyalty, particularly among millennial and Gen Z consumers. Another strong opportunity is in emerging markets such as Southeast Asia, Africa, and Latin America. These regions are witnessing rising disposable incomes, urbanization, and youth-driven demographics, all of which are fueling demand for personal care products. Affordable, locally relevant formulations supported by strong digital marketing can make significant inroads in these underserved yet high-potential markets. Additionally, wellness-oriented personal care—combining mental well-being, stress relief, and self-care—has opened a new dimension. Products with aromatherapy benefits, soothing textures, or functional actives like adaptogens and CBD are increasingly sought after. There’s also a notable opportunity in male grooming, a previously underdeveloped segment now seeing exponential growth, particularly in beard care, skincare, and fragrances tailored for men. Furthermore, the rise of inclusive beauty—products that cater to diverse skin tones, hair textures, and gender identities—presents both a commercial and social impact opportunity. Brands that authentically embrace diversity in product development and marketing are poised to gain broader acceptance and loyalty. Finally, strategic partnerships with tech firms, biotech labs, and environmental NGOs can lead to innovations in smart skincare devices, sustainable ingredient sourcing, and carbon-neutral production practices. Together, these opportunities represent the next frontier of growth for the personal care industry.

PERSONAL CARE MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 - 2030 |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2030 |

|

CAGR |

5.2% |

|

Segments Covered |

By Product, application, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

L'Oréal, Procter & Gamble, Unilever, Estée Lauder, and Johnson & Johnson. |

Personal Care Market segmentation

• Skincare

• Haircare

• Oral Care

• Deodorants and Fragrances

• Cosmetics and Makeup

• Hygiene Products

• Men’s Grooming Products

• Baby and Child Care

Skincare is the most dominant segment in the global personal care market, owing to increasing awareness about skin health, anti-aging, sun protection, and routine care. Skincare alone accounts for over 35% of the market. Innovations such as serums, facial oils, and dermatologically-tested products have fueled the demand. The segment benefits from strong consumer interest, constant product launches, and an ability to cater to diverse needs across age, gender, and skin types. Social media influencers and dermatologists contribute to continuous engagement and consumer education in this category.

• Household/Individual Use

• Salons and Spas

• Online Subscription Boxes

• Travel and Hospitality

• Dermatology Clinics

• E-commerce Platforms (D2C)

Household or individual use remains the most dominant application segment due to the personal and routine nature of care products. Most consumers purchase personal care products for at-home use, forming habits around daily hygiene and grooming. This segment includes everything from toothpaste and shampoo to facial creams and deodorants. It benefits from high purchase frequency, brand loyalty, and increasing customization for home-use regimens. The shift to work-from-home has further accelerated demand for at-home self-care products.

• North America

• Europe

• Asia-Pacific

• South America

• Middle East and Africa

Asia-Pacific is the dominant region in the global personal care market, contributing to more than one-third of total global revenues in 2024. This dominance is supported by several structural and cultural factors. The region is home to large, densely populated countries like China and India, where rising disposable income, urbanization, and youth demographics drive strong demand for personal care products. Additionally, cultural importance placed on grooming and skincare in countries like South Korea and Japan fuels innovation and early adoption of new trends. K-beauty and J-beauty are now globally recognized for their innovation, minimalistic regimens, and efficacy, influencing product development worldwide. The rise of local and regional brands that understand consumer preferences, such as skin tone-specific products or herbal formulations, further supports domestic consumption. E-commerce penetration and mobile-first consumer behavior have also created robust digital sales channels, helping global and local brands alike. Meanwhile, the expansion of organized retail chains and beauty specialty stores in tier-2 and tier-3 cities enhances accessibility and visibility. Governments in the region are also encouraging manufacturing through policies and incentives, turning countries like India into major production hubs. All these factors together position Asia-Pacific as both the largest and the fastest-growing region in the personal care market.

The COVID-19 pandemic brought both challenges and transformation to the global personal care market. In the initial months of the pandemic, the industry experienced supply chain disruptions, labor shortages, and reduced retail footfall due to lockdowns and safety concerns. Demand for certain product categories such as makeup and fragrances declined temporarily as consumers stayed indoors and socialized less. However, other categories like hygiene products, skincare, and haircare saw significant growth as people turned to self-care and preventive health routines. The shift to remote work and increased time spent at home accelerated the use of skincare and wellness-related personal care items. DIY beauty treatments, home facials, and self-grooming became new habits. Meanwhile, digital sales surged as consumers increasingly shopped online. Brands that adapted quickly to digital-first strategies, strengthened e-commerce channels, and engaged through content marketing were able to maintain customer engagement and drive sales. The pandemic also heightened consumer awareness about product ingredients, safety, and sustainability, reinforcing demand for clean and natural personal care options. Supply chain resilience became a focal point for companies, with many seeking to localize manufacturing and build agile distribution networks. New hygiene-focused product lines such as antibacterial lotions and facial cleansers became permanent additions to brand portfolios. COVID-19 also accelerated the wellness trend, blurring lines between personal care, healthcare, and mental well-being. Overall, while the market faced short-term disruptions, the pandemic catalyzed lasting shifts in consumer behavior, product innovation, and go-to-market strategies that continue to shape the industry’s trajectory.

Latest trends/Developments

The personal care market is witnessing a wave of trends that are reshaping product innovation, branding, and consumer engagement. One prominent trend is the evolution of the wellness-centric personal care routine, where mental and emotional well-being are integrated into skincare and grooming rituals. Products infused with adaptogens, essential oils, and calming botanicals are in demand, offering both aesthetic and psychological benefits. Another trend gaining momentum is the use of biotechnology to create bio-based actives and lab-grown ingredients that offer high efficacy with minimal environmental impact. Companies are partnering with biotech firms to develop next-generation solutions for aging, acne, and sensitivity. Gender-neutral and inclusive beauty is another critical development, with brands launching products that cater to diverse skin tones, hair textures, and gender identities. Packaging design and brand language are also evolving to reflect this inclusivity. Personalized beauty continues to rise with AI-driven diagnostics, DNA-based product matching, and personalized subscription kits gaining traction. Augmented reality features such as virtual try-ons and face mapping tools enhance consumer confidence in online purchases. The clean beauty movement has matured, with consumers expecting not just chemical-free formulations but also ethical sourcing, carbon-neutral production, and full ingredient transparency. Waterless and solid personal care products are becoming popular for their environmental benefits and travel-friendliness. Influencer-led brands and celebrity collaborations remain impactful, but authenticity and brand values are now key to consumer loyalty. Finally, regional heritage and traditional remedies are being reinterpreted with modern science, giving rise to hybrid products that blend tradition with innovation.

Key Players:

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

The Global Personal Care Market was valued at USD 510 billion in 2024 and will grow at a CAGR of 5.2% from 2025 to 2030. The market is expected to reach USD 657.13 billion by 2030.

Key drivers include rising health and beauty awareness, growth in e-commerce, and demand for clean and sustainable products

Segments include skincare, haircare, cosmetics, hygiene products, oral care, men’s grooming, and baby care.

Asia-Pacific is the dominant region due to large populations, cultural grooming traditions, and rising disposable incomes.

Leading players include L'Oréal, Procter & Gamble, Unilever, Estée Lauder, and Johnson & Johnson.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.