Global Enterprise Data Catalog Market Research Report - Segmented By Organization Size (Small and Medium Enterprises (SMEs) and Large Enterprises); By Deployment Mode (On-Premises and Cloud Based); By End User Industry (BFSI, Healthcare, Retail & eCommerce, IT & Telecommunication, Manufacturing, and Others); and Region - Size, Share, Growth Analysis | Forecast (2024 – 2030)

Enterprise Data Catalog Market Size (2024 – 2030)

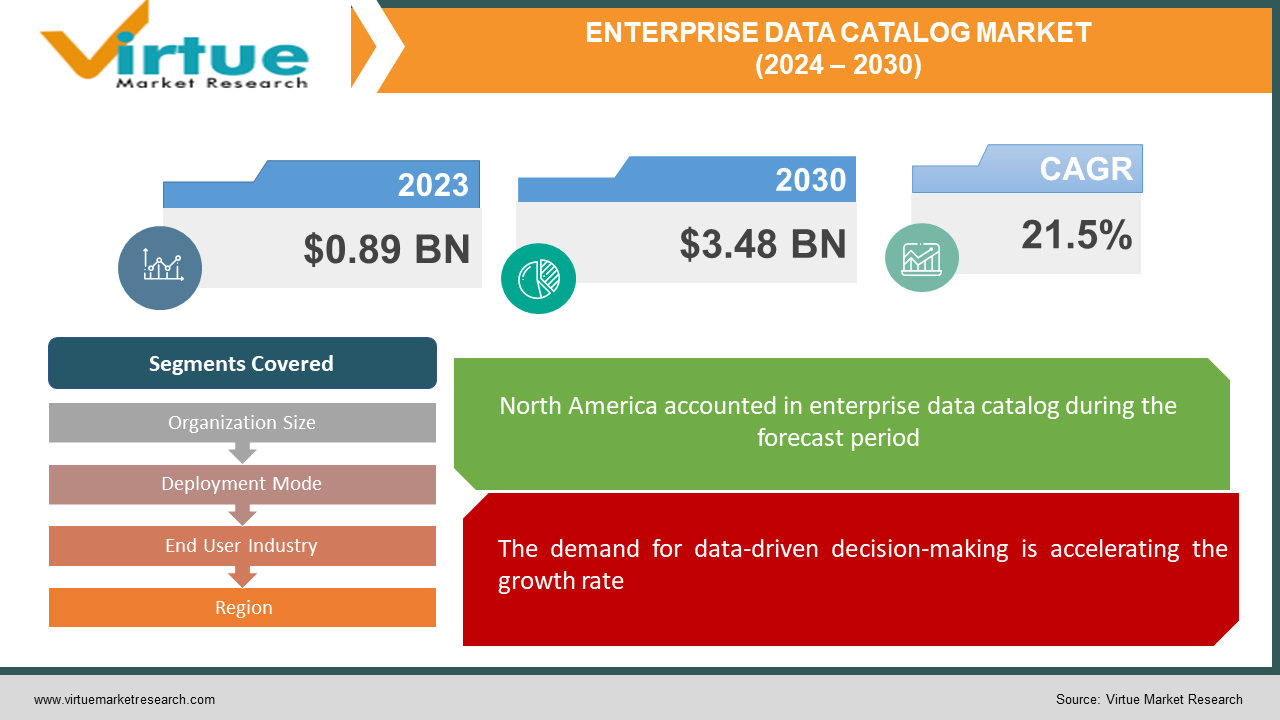

The market for enterprise data catalog at the global level is expanding quickly; it was estimated to be worth 0.89 USD billion in 2023 and is expected to increase to 3.48 USD billion by 2030, with a projected compound annual growth rate (CAGR) of 21.5% from 2024 to 2030.

Due to the increasing demand for efficient data management solutions across numerous industries, the market for enterprise data catalogs, or EDCs, is rising quickly. Because of the ever-increasing volume and complexity of data that organizations must deal with, the EDC market is now crucial to achieving their digital transformation objectives. EDC solutions assist companies in enhancing their data governance, analytics, and compliance capabilities by locating, organizing, and managing massive data sources. The market is growing due to multiple factors, including the proliferation of data-driven decision-making, regulatory regulations necessitating complex data management procedures, and the growing usage of cloud-based technology. Additionally, as companies recognize the intrinsic worth of their data, they are searching for advanced cataloging solutions to unlock insights, increase operational effectiveness, and foster innovation.

Key Market Insights:

The need for strong security measures like encryption and access restrictions is highlighted by rising concerns about data security and privacy, which present substantial obstacles to market development. Promising potential arises from the integration of machine learning (ML) and artificial intelligence (AI) technologies, which enable automated data classification, discovery, and metadata enrichment for improved accuracy and efficiency in data cataloging operations.

North America is the market leader because of its strong legal systems and early adoption of cutting-edge data management technologies, which have significantly fueled industry expansion. As a result of its developing digital economy and rising use of data analytics tools across a range of industries, the Asia-Pacific region is showing the quickest growth rate, indicating enormous potential for market expansion in the area.

Global Enterprise Data Catalog Market Drivers:

The demand for data-driven decision-making is accelerating the growth rate.

In the contemporary digital era, organizations are leaning more and more on data to guide their strategic decision-making processes. The need for businesses to make effective use of their data resources is what is driving the market for enterprise data catalogs, or EDCs. Businesses may organize and catalog massive volumes of data from numerous sources with the use of EDC solutions, providing a coherent picture that aids in well-informed decision-making. Through the ability to identify trends, anticipate future occurrences, and unearth significant insights, EDC solutions help businesses gain a competitive edge in the global economy and enhance their business intelligence skills.

The increasing need for data governance solutions is facilitating the expansion.

Because data privacy regulations and compliance requirements are becoming more widespread worldwide, businesses are under increasing pressure to ensure the security and integrity of their data assets. The need for robust data governance solutions that support companies in adhering to legal requirements while maintaining operational efficacy is what's propelling the enterprise data catalog, or EDC, market. Businesses may adhere to data governance policies and reduce the likelihood of breaking the law with the aid of EDC systems' access control mechanisms, metadata management, and data lineage tracking features. As regulatory scrutiny grows, there is an increasing requirement for EDC solutions that prioritize data governance and compliance capabilities.

The shift to agile and scalable data management solutions through cloud adoption is enabling their development.

The growing adoption of cloud computing is reshaping the market for enterprise data catalogs (EDCs) as companies seek scalable and adaptable solutions to manage their expanding data ecosystems. Cloud-based EDC platforms offer several advantages, including elastic scalability, reduced infrastructure expenses, and expedited implementation. Using the scalability and flexibility of cloud infrastructures, businesses may easily expand their data cataloging capabilities to suit growing data volumes and shifting business needs. Additionally, cloud-based EDC systems provide seamless integration with other cloud services and data analytics tools, maximizing the value of data assets for enterprises while cutting down on overhead. As more businesses use cloud-native technology, it is projected that demand for cloud-based EDC solutions will increase.

Global Enterprise Data Catalog Market Restraints and Challenges:

Data security is a major concern.

One of the primary challenges confronting the global enterprise data catalog (EDC) market is the growing concern over data security and privacy. Organizations that collect and catalog vast amounts of data are more susceptible to data breaches, cyberattacks, and illegal access. The decentralized nature of data cataloging, which spreads information over multiple platforms and systems, makes security measures more challenging. Strong security measures, like encryption, access controls, and data masking strategies, are required to solve these issues and shield private information from possible attackers. If data security issues are not appropriately addressed, organizations run the risk of suffering financial loss, damage to their brand, and noncompliance with rules, among other major consequences.

Data quality is another barrier.

The global enterprise data catalog (EDC) industry is beset with numerous data quality concerns, including errors, duplication, and inconsistencies. Poor data quality can undermine the success of data categorization initiatives by resulting in inaccurate conclusions, poor judgment, and decreased operational efficiency. To maintain data accuracy and consistency, data cataloging solutions need to incorporate procedures for data cleansing, deduplication, and normalization. Organizations must set up procedures and structures for data governance to maintain standards for data quality and carry out regular evaluations of data integrity. Businesses may increase the dependability and usefulness of their data cataloging efforts and the value they derive from their data assets by proactively addressing data quality issues.

Interoperability difficulties in diverse data ecosystems create complexities.

Due to the difficulty of integrating Enterprise Data Catalogue (EDC) systems with existing IT infrastructures, organizations seeking to effectively leverage data cataloging capabilities face significant challenges. System integration is challenging because businesses usually operate in disparate contexts with a variety of data sources, formats, and technologies. Integration problems caused by disparate data silos, outdated systems, and incompatible data formats can impair the scalability and interoperability of EDC solutions. To solve these problems, facilitate data exchange, and expedite the data cataloging process, organizations need to invest in integration technologies like connectors, APIs, and middleware. By negotiating the difficulties of integrating EDC solutions into their current infrastructure, organizations may also maximize the value of their data.

Global Enterprise Data Catalog Market Opportunities:

AI and ML have been providing the market with many possibilities.

In the worldwide enterprise data catalog (EDC) market, combining machine learning (ML) and artificial intelligence (AI) technologies has a lot of potential. By automating tasks linked to data discovery, classification, and metadata enrichment, EDC platforms may improve accuracy and efficiency with the use of these advanced features. By employing AI and ML technology, organizations can discover hidden insights in their data, automate data governance procedures, and discover connections across many datasets. AI-driven data cataloging systems may also adapt and develop over time, which will increase their value and efficacy in dynamic data environments. By applying AI and ML, organizations may enhance their data cataloging capabilities, streamline data management processes, and gain insightful knowledge to drive business growth.

Increasing the use of data governance and compliance while meeting industry standards and regulatory requirements has been beneficial.

Because industry norms and laws are changing, there is a significant opening in the market for global enterprise data catalogs or EDCs. There is growing demand for businesses across several industries to comply with industry-specific norms and regulations, in addition to stringent data privacy laws such as HIPAA, CCPA, and GDPR. EDC solutions offer robust data governance and compliance features, like metadata management, data lineage tracing, and access restrictions, to help businesses achieve regulatory compliance and risk reduction. Through the centralization of data cataloging processes and the enforcement of governance standards, EDC solutions assist businesses in maintaining data integrity, ensuring accountability, and demonstrating regulatory compliance to stakeholders and regulatory bodies. Data governance and compliance features are projected to become more and more important in EDC solutions as regulatory requirements continue to

Unlocking unstructured data's potential is augmenting market growth.

Because there is a wealth of unstructured data, the worldwide enterprise data catalog (EDC) market has a tremendous opportunity for innovation and growth. The majority of data generated by organizations is unstructured and consists of textual records, multimedia files, and social media posts. EDC systems with advanced text mining, natural language processing (NLP), and content analysis tools enable businesses to catalog, categorize, and analyze unstructured data alongside structured datasets. By utilizing insights from a range of data sources, organizations may gain a thorough awareness of their data environment, uncover hidden patterns, and derive actionable insights to inform decisions and advance business objectives.

ENTERPRISE DATA CATALOG MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2023 - 2030

Base Year

2023

Forecast Period

2024 - 2030

CAGR

21.5%

Segments Covered

By Organization Size, Deployment Mode, End User Industry, and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Enterprise Data Catalog Market Segmentation: By Organization Size

Small and Medium Enterprises (SMEs)

Large Enterprises

Large enterprises are the largest growing organization size. Strong data management solutions are required for these organizations since they handle enormous amounts of data from many sources and business divisions. Enterprise data catalogs enable large enterprises to accomplish regulatory compliance, foster cross-team cooperation, and accomplish full data governance. SMEs are the fastest-growing category. This is because SMEs are realising how important data management solutions are to boosting productivity and competitiveness. SMEs use business data catalogs to improve decision-making processes, expedite data discovery, and increase data quality despite their smaller size. SMEs use data to drive development and innovation through affordable, scalable solutions that are customized to meet their needs. This allows them to quickly respond to changing market conditions and take advantage of new possibilities.

Enterprise Data Catalog Market Segmentation: By Deployment Mode

On-Premises

Loud Based

Cloud-based solutions emerge as the largest and fastest-growing deployment mode. Businesses all over the world are growing more and more interested in cloud-based deployment due to its unparalleled advantages, which include scalability, agility, and cost-effectiveness. Unlike traditional on-premises solutions, cloud-based EDC platforms do not require ongoing maintenance or upfront infrastructure investments, allowing businesses to swiftly extend their data cataloging capabilities as needed. In today's fast-paced corporate environment, where businesses must deal with shifting workloads and data management requirements, this adaptability is very helpful.

Enterprise Data Catalog Market Segmentation: By End User Industry

BFSI

Healthcare

Retail & eCommerce

IT & Telecommunication

Manufacturing

Others

The BFSI sector is the largest growing. BFSI organizations give regulatory compliance, risk management, and data governance top priority since they have access to enormous volumes of sensitive financial data. Because they offer a centralized platform for lineage tracking, metadata management, and data discovery, enterprise data catalogs are essential in this field. BFSI companies may improve regulatory reporting capabilities, guarantee data integrity, and boost operational efficiency by utilizing modern data catalog solutions. Furthermore, BFSI institutions use enterprise data catalogs to extract actionable insights from their data assets in response to the growing demand for individualized financial services and the rise of fintech disruptors. This allows them to provide better customer experiences, reduce risks, and stay ahead of the competition in the quickly changing financial landscape. The retail & e-commerce sector is the fastest-growing end-user. With the use of EDC systems, these companies can effectively handle and analyze massive volumes of customer data, transactional records, inventory information, and marketing analytics. By implementing EDC platforms made especially for the retail sector, including supply chain optimization, personalized product recommendations, and consumer behavior research, retailers may increase their competitiveness and enhance customer experiences.

Enterprise Data Catalog Market Segmentation: Regional Analysis

North America

Europe

Asia-Pacific

South America

Middle East & Africa

North America is the largest growing market. Strong legislative frameworks, the presence of leading technology companies, and the region's early adoption of cutting-edge data management solutions all contribute to its leadership position. North America is positioned as a major engine for market development and innovation due to the region's thriving ecosystem of technology suppliers and strong demand for advanced data analytics solutions, which further drive the adoption of corporate data catalogs. Asia-Pacific is expanding at the fastest rate due to the region's growing digital economy and rising use of data analytics tools. Businesses in industries including banking, telecommunications, and e-commerce use business data catalogs to make better decisions, increase operational efficiency, and extract insights from massive amounts of data. Additionally, as big data and cloud computing become more widespread, businesses in Asia-Pacific are embracing data catalog solutions to use their data assets for competitive advantage and market differentiation.

COVID-19 Impact Analysis on the Enterprise Data Catalog Market:

The COVID-19 epidemic has had a major impact on the sector, presenting both opportunities and challenges. On the one hand, the sudden shift to remote work and digital operations has accelerated the adoption of cloud-based EDC solutions as businesses search for adaptable and scalable data management solutions to support distant teams and ensure business continuity. The pandemic has also brought attention to how important it is to make choices on data, which has led to increased investments in EDC platforms to improve data governance, boost analytics capabilities, and foster operational efficiencies. However, due to budgetary constraints and economic worries, several organizations have chosen to postpone or scale back their IT investments, which has impacted the pace at which EDC adoption is happening in some cases. Furthermore, because of the disruption to supply chains and worker dynamics, which has increased the importance of data security and privacy, businesses are giving priority to EDC solutions that offer robust security features and compliance capabilities. All things considered, the COVID-19 pandemic has caused challenges for the EDC sector, but it has also presented an opportunity for suppliers to exercise creativity and adjust to the ever-changing demands of their customers in the rapidly evolving business landscape.

Latest Trends/ Developments:

Due to several recent developments that are altering the analytics and data management landscape, the market for enterprise data catalogs (EDCs) is growing swiftly. One noteworthy trend is the increasing integration of artificial intelligence (AI) and machine learning (ML) technologies in EDC platforms. Organizations that use AI and ML algorithms to automate data discovery, classification, and metadata tagging processes can expedite data cataloging efforts and more efficiently extract pertinent insights from their data assets.

This trend reflects both the increasing complexity of modern IT settings and the need for flexible and interoperable data management solutions. Furthermore, businesses are discovering they can extract valuable intelligence and insightful information from their data catalogs by combining advanced analytics and visualization tools with EDC platforms. Taken together, these latest developments and trends demonstrate how the EDC sector is constantly evolving and how data management strategies are constantly altering to become more creative, effective, and adaptable.

Key Players:

Collibra

Alation

Informatica

IBM

Microsoft

SAP

Waterline Data

TIBCO Software

Talend

Denodo

To Learn more about this report,

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. ENTERPRISE DATA CATALOG MARKET – Scope & Methodology

1.1 Market Segmentation

1.2 Scope, Assumptions & Limitations

1.3 Research Methodology

1.4 Primary Sources

1.5 Secondary Sources Chapter 2. ENTERPRISE DATA CATALOG MARKET – Executive Summary

2.1 Market Size & Forecast – (2024 – 2030) ($M/$Bn)

2.2 Key Trends & Insights

2.2.1 Demand Side

2.2.2 Supply Side

2.3 Attractive Investment Propositions

2.4 COVID-19 Impact Analysis Chapter 3. ENTERPRISE DATA CATALOG MARKET – Competition Scenario

3.1 Market Share Analysis & Company Benchmarking

3.2 Competitive Strategy & Development Scenario

3.3 Competitive Pricing Analysis

3.4 Supplier-Distributor Analysis Chapter 4. ENTERPRISE DATA CATALOG MARKET Entry Scenario

4.1 Regulatory Scenario

4.2 Case Studies – Key Start-ups

4.3 Customer Analysis

4.4 PESTLE Analysis

4.5 Porters Five Force Model

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Powers of Customers

4.5.3 Threat of New Entrants

4.5.4 Rivalry among Existing Players

4.5.5 Threat of Substitutes Chapter 5. ENTERPRISE DATA CATALOG MARKET – Landscape

5.1 Value Chain Analysis – Key Stakeholders Impact Analysis

5.2 Market Drivers

5.3 Market Restraints/Challenges

5.4 Market Opportunities Chapter 6. ENTERPRISE DATA CATALOG MARKET – By Organization Size

6.1 Introduction/Key Findings

6.2 Small and Medium Enterprises (SMEs)

6.3 Large Enterprises

6.4 Y-O-Y Growth trend Analysis By Organization Size

6.5 Absolute $ Opportunity Analysis By Organization Size, 2024-2030 Chapter 7. ENTERPRISE DATA CATALOG MARKET – By End User

7.1 Introduction/Key Findings

7.2 BFSI

7.3 Healthcare

7.4 Retail & eCommerce

7.5 IT & Telecommunication

7.6 Manufacturing

7.7 Others

7.8 Y-O-Y Growth trend Analysis By End User

7.9 Absolute $ Opportunity Analysis By End User, 2024-2030 Chapter 8. ENTERPRISE DATA CATALOG MARKET – By Deployment Mode

8.1 Introduction/Key Findings

8.2 On-Premises

8.3 Loud Based

8.4 Y-O-Y Growth trend Analysis By Deployment Mode

8.5 Absolute $ Opportunity Analysis By Deployment Mode, 2024-2030 Chapter 9. ENTERPRISE DATA CATALOG MARKET , By Geography – Market Size, Forecast, Trends & Insights

9.1 North America

9.1.1 By Country

9.1.1.1 U.S.A.

9.1.1.2 Canada

9.1.1.3 Mexico

9.1.2 By Organization Size

9.1.3 By End User

9.1.4 By Deployment Mode

9.1.5 Countries & Segments - Market Attractiveness Analysis

9.2 Europe

9.2.1 By Country

9.2.1.1 U.K

9.2.1.2 Germany

9.2.1.3 France

9.2.1.4 Italy

9.2.1.5 Spain

9.2.1.6 Rest of Europe

9.2.2 By Organization Size

9.2.3 By End User

9.2.4 By Deployment Mode

9.2.5 Countries & Segments - Market Attractiveness Analysis

9.3 Asia Pacific

9.3.1 By Country

9.3.1.1 China

9.3.1.2 Japan

9.3.1.3 South Korea

9.3.1.4 India

9.3.1.5 Australia & New Zealand

9.3.1.6 Rest of Asia-Pacific

9.3.2 By Organization Size

9.3.3 By End User

9.3.4 By Deployment Mode

9.3.5 Countries & Segments - Market Attractiveness Analysis

9.4 South America

9.4.1 By Country

9.4.1.1 Brazil

9.4.1.2 Argentina

9.4.1.3 Colombia

9.4.1.4 Chile

9.4.1.5 Rest of South America

9.4.2 By Organization Size

9.4.3 By End User

9.4.4 By Deployment Mode

9.4.5 Countries & Segments - Market Attractiveness Analysis

9.5 Middle East & Africa

9.5.1 By Country

9.5.1.1 United Arab Emirates (UAE)

9.5.1.2 Saudi Arabia

9.5.1.3 Qatar

9.5.1.4 Israel

9.5.1.5 South Africa

9.5.1.6 Nigeria

9.5.1.7 Kenya

9.5.1.8 Egypt

9.5.1.9 Rest of MEA

9.5.2 By Organization Size

9.5.3 By End User

9.5.4 By Deployment Mode

9.5.5 Countries & Segments - Market Attractiveness Analysis Chapter 10. ENTERPRISE DATA CATALOG MARKET – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments)

10.1 Collibra

10.2 Alation

10.3 Informatica

10.4 IBM

10.5 Microsoft

10.6 SAP

10.7 Waterline Data

10.8 TIBCO Software

10.9 Talend

10.10 Denodo

Fill out the form below and our team will get back to you shortly

FAQ's

The global market for enterprise data catalogs is growing rapidly; it is forecast to reach 3.48 billion USD by 2030, with a compound annual growth rate (CAGR) of 21.5% from 2024 to 2030. In 2023, the market was valued at 0.89 billion USD.

The need for effective data management solutions is being driven primarily by the growing volume and complexity of data in organizations, which is driving the global enterprise data catalog market.

The primary challenge facing the worldwide enterprise data catalog market is the prevalence of data quality issues, including errors, duplicates, and inconsistencies.

In 2023, North America held the largest share of the global enterprise data catalog market.

The major participants in the global enterprise data catalog market are Colibra, Alignment, Informatica, IBM, Microsoft, SAP, Waterline Data, TIBCO Software, Talend, Denodo, Zaloni, and Astacama.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-203 | Published Date: July 2025 | Format: Excel and PDF

The 3D Scanning Market was valued at USD 2.28 billion in 2024 and is projected to reach a market size of USD 5.37 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CA...

Report Code: VMR-14818 | Published Date: July 2024 | Format: Excel and PDF

The Global Passwordless Authentication Market is expected to grow from USD 22.70 billion in 2025 to approximately USD 49.13 billion by 2030, at a 16.7% CAGR from 2026-2030.

Report Code: VMR-435 | Published Date: March 2024 | Format: Excel and PDF

The Equity Management Software Market was valued at USD 591.85 million in 2023. Over the forecast period of 2024-2030, it is projected to reach USD 1508.47 million by 2030, growing at a CAGR of 14.3%.

Report Code: VMR-15816 | Published Date: March 2024 | Format: Excel and PDF

The global intellectual property (IP) services market was valued at USD 2.8 billion and is projected to reach a market size of USD 6.38 billion by the end of 2030. Over the forecast period of 2024–2030, the market is pro...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”