Central Bank Digital Currency (CBDC) Market Research Report – Segmented By type (Wholesale CBDC and Retail CBDC); By issuance (Direct CBDC, Indirect CBDC and Hybrid CBDC); By structure (Account-based and token-based), and Region- Size, Share, Growth Analysis | Forecast (2024 – 2030)

Central Bank Digital Currency (CBDC) Market Size (2024 – 2030)

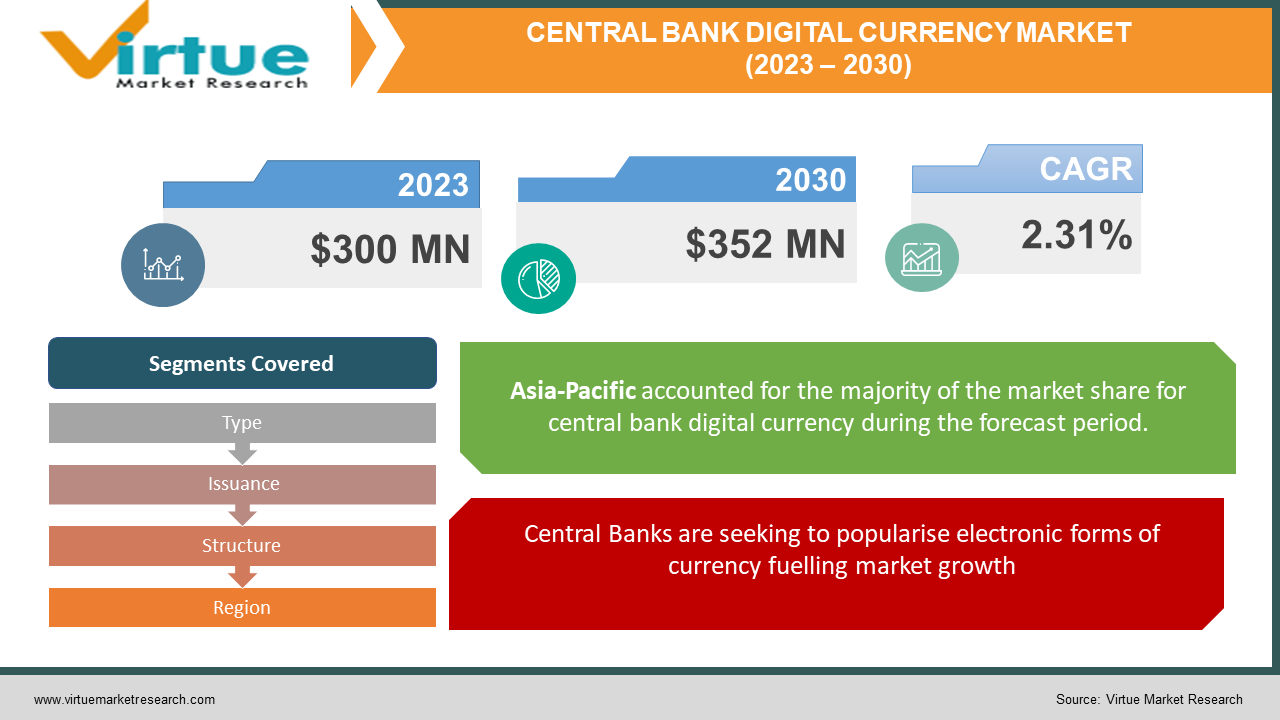

The Central Bank Digital Currency Market was valued at USD 300 Million in 2023 and is projected to reach a market size of USD 352 Million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 2.31%.

According to the definition given by the central bank, digital currencies are those that are issued by the bank and are connected to the country's currency. It is a digital equivalent of fiat money in the digital economy. The central bank, government-approved organizations, or both run the database that serves as its foundation. The database must be used in order to monitor CBDC flow. The main goals of CBDCs for businesses and customers alike are financial security, accessibility, privacy, transferability, and ease of use.

Key Market Insights

Nine out of ten central banks are investigating CBDCs, and more than half of them are actively creating or conducting actual trials with them, according to a survey report published by Banking International Settlements (BIS). More specifically, the process of establishing retail CBDCs has advanced. Moreover, a staggering 90% of the central banks included in the survey are working on CBDC initiatives. Overall, the research provides valuable insights into central banks' use of digital money and the path of monetary policy. Sixty-four countries make up the new high for the number of countries in the advanced phase of exploration (launch, pilot, or development).The Reserve Bank of India (RBI) in India has been investigating and studying the possibilities of CBDCs for a considerable amount of time. On December 1, 2022, they also started the first pilot program for the Digital Rupee- Retail segment (e₹-R).

Central Bank Digital Currency Market Drivers:

Central Banks are seeking to popularise electronic forms of currency fuelling market growth.

Payment and settlement systems have made it possible for the common individual to access a vast array of digital opportunities, demonstrating how the globe is embracing the digital revolution. In order to complete a transaction, clients have a wide range of options to choose from these days. They select a payment method depending on the value they believe it has in a certain situation because each payment mechanism has a specific role and purpose. The shift from cash to electronic payments leads to an increased reliance on electronic payment systems, which impacts the payment environment's resilience and diversity. With the use of paper smoney decreasing, central banks hope to encourage a more widely recognized electronic form of payment. Using a lot of real currency, jurisdictions want to improve the effectiveness of their issuance procedures.

Among the countries that were inspired to adopt CBDC were the Bahamas and the Caribbean, which are made up of a huge number of tiny and large islands. The growing use of private virtual currencies indicates the public's desire for digital currencies, which central banks seek to balance while sidestepping the more problematic aspects of such currencies.

The dangers of utilizing cryptocurrencies, or digital currency, as they exist now would be diminished by CBDCs.

The risks associated with using cryptocurrencies and digital currencies in their current form would be reduced with the introduction of CBDCs. The value of cryptocurrencies is constantly fluctuating and quite unpredictable. This volatility may have a negative effect on the overall stability of an economy and severely strain the finances of many households. Thanks to CBDCs, which are supported by the government and governed by a central bank, individuals, businesses, and houses would all have a safe way to exchange digital cash.

Central Bank Digital Currency Market Restraints:

CBDCs might be subjected to cyber hacks which might lead to server blockages unforced timeouts or service declines.

Cyberattacks that target CBDCs may cause unexpected timeouts, server outages, or a decline in service quality. CBDC may also be susceptible to other cyberthreats, the principal ones being distributed denial-of-service (DDoS) attacks that disrupt services, supply-side attacks directed at infrastructure, and side-channel attacks on user devices and payment apps. DLT-based CBDC systems are vulnerable to DDoS assaults since each transaction in these systems necessitates communication with every other node on the network. The goal of a denial-of-service (DDoS) assault is to overload a server or network with too much traffic in too short a period of time, causing it to crash. If the government does not address these cyberattacks, the public's trust in the ecosystem will be weakened and the integrity of the CBDC system endangered.

inclusive tool by utilising innovation to remove the barriers, just like with offline payments.

Central Bank Digital Currency Market Opportunities:

The sudden spike in interest in CBDC can be attributed to central banks' perception of its importance in advancing public policy objectives, maintaining economic stability, and providing individuals with a convenient, secure, and reliable payment medium.

Every country has a different approach to implementing CBDC. Others are conducting research and testing iterations to gradually develop their CBDC, while some countries are speeding towards implementation. To determine when and how CBDC can be implemented, discussions and activities are now underway in India. Consequently, this will give all players in the ecosystem far more chances to create services that streamline and ease digital payment processing and citizen transactions for a variety of use cases and requirements.

Financial inclusion is described as a desired outcome of retail CBDC projects, which appear increasingly developed in emerging economies. In more developed nations with sophisticated financial markets and interbank networks, the bulk of wholesale activities occur.

CENTRAL BANK DIGITAL CURRENCY MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2023 - 2030

Base Year

2023

Forecast Period

2024 - 2030

CAGR

2.31%

Segments Covered

By Type, Issuance, Structure, and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

Company 1, Company 2, Company 3 Company 4, Company 5, Company 6

Central Bank Digital Currency Market Segmentation: By Type

Wholesale CBDC

Retail CBDC

A 2021 survey conducted by the Bank for International Settlements (BIS) found that 14% of central banks globally were putting trial programmes into place, 60% were testing the technology, and 86% of central banks globally were actively looking into the feasibility of utilising CBDCs. Financial inclusion is described as a desired outcome of retail CBDC projects, which appear increasingly developed in emerging economies. In more developed nations with sophisticated financial markets and interbank networks, the bulk of wholesale activities occur.

Retail CBDC is the term for the digital form of fiat money that is meant for average consumers and used by everyday people for daily financial activities. Distributed ledger technology (DLT) functions like a privately controlled blockchain network under government supervision, permitting transaction tracking while safeguarding identities. Furthermore, it diminishes the power of private entities, discouraging deception and other unlawful activities.

Wholesale CBDC can be very helpful in the development of wholesale payments, which central banks are trying to modernise. Wholesale CBDC will permit net-basis interbank settlements. It will also make the conditionality of payment easier, which is the process of paying off a debt subject to the performance of a duty or the delivery of an asset or security. The use of wholesale CBDC can help financial markets, interbank payments, and cross-border remittances making it the fastest-growing segment during the forecasted years.

Central Bank Digital Currency Market Segmentation: By Issuance

Direct CBDC

Indirect CBDC

Hybrid CBDC

The two models utilised for the issue and management of CBDCs are the Direct Model (Single Tier model) and the Indirect Model (Two-Tier model). Under an indirect approach, a central bank and other intermediaries, like banks and other service providers, each have their own unique role. In this structure, the central bank does not directly issue CBDC to customers through intermediaries; rather, it just oversees wholesale payments to intermediaries. It is anticipated to be both the largest and the fastest growing segment during the outlook period due to this.

Central Bank Digital Currency Market Segmentation: By Structure

Account-based

Token-based

A token-based CBDC is regarded as a bearer instrument, much like banknotes, and is thought to belong to the person holding the tokens at any given time. However, an account-based system would have to maintain track of all CBDC holders' balances, transactions, and ownership of the funds. Moreover, in a token-based CBDC, the recipient of the token must attest that he actually is the token's owner; in an account-based CBDC, an intermediary verifies the identity of an account holder. Although both types of CBDCs have advantages, token-based CBDCs are seen to be a superior choice for CBDC-R due to their resemblance to real cash; nevertheless, account-based CBDCs may also be a viable option for CBDC-W.Because account-based and token-based languages do not create categories that are mutually exclusive, they present challenges when used for digital payments. If a taxonomic hierarchy of digital payment systems were to be defined, members of the higher taxonomic rank would not be separated by these terms.

Central Bank Digital Currency Market Segmentation: Regional Analysis

North America

Asia-Pacific

Europe

South America

Middle East and Africa

A total of 130 countries, accounting for 98% of global GDP, are examining CBDCs. By May 2020, there were only 35 countries considering creating a CBDC. 64 countries are involved in advanced exploration, which include development, piloting, or launch, breaking previous records. Currently, CBDC development is at an advanced stage in 19 of the G20 countries. Nine of those are currently part of pilot projects. Nearly all of the G20 countries have made substantial progress on these projects and contributed new financing in the last six months. Eleven countries have fully implemented digital currency. More than 200 scenarios are being investigated for China's pilot programme, which currently covers 260 million people, including public transport, stimulus payments, and e-commerce. The European Central Bank plans to launch a digital euro pilot programme shortly. More than 20 more countries will start getting ready to pilot their CBDCs in 2023. Thailand, Australia, and Russia intend to do additional pilot testing. India and Brazil want to make their debuts in 2024. In the US, retail CBDC development has come to an end. Conversely, other G7 banks, like the Bank of England and the Bank of Japan, are developing CBDC prototypes and offering advice to the public and private sectors regarding financial stability and privacy. However, the US is moving forward with a wholesale CBDC (bank-to-bank).Wholesale CBDC innovations have accelerated after the G7 sanctions response to Russia's invasion of Ukraine. Currently, twelve efforts for cross-border wholesale CBDC are active.

COVID-19 Impact Analysis on the Central Bank Digital Currency Market:

The Bank for International Settlements believes that the COVID-19 crisis' effects on retail payments will help central banks build digital currencies. First, the study draws attention to the sharp decline in cash payments brought on by shop and customer concerns about virus propagation. The "precautionary holdings" of cash resulting from economic uncertainty have led to a decline in daily cash transactions. In tandem with this, national government regulations like eliminating physical stores have resulted in an increase in e-commerce payments. Due to decreased mobility, there has been a significant decline in both the volume of cross-border visa transactions and migrant remittances. All of these changes, in BIS's opinion, emphasise the advantages and drawbacks of the current payment methods. On the one hand, digital payments have enabled the continuation of numerous economic operations, although causing major disruptions to daily living. However, the crisis has made already-existing socioeconomic divides more pronounced, in part because of unequal financial inclusion, which may make it more difficult for some people to qualify for government assistance: Demands for future payment services that are more affordable and inclusive as well as for vulnerable communities to have more access to digital payments have increased as a result of the crisis.

Latest Trends/ Developments:

Japan plans to host a CBDC forum and extend an invitation to private enterprises engaged in retail payments or related technologies to participate in the discourse. Based on the data, the bank will decide by 2026 whether to launch a digital currency.

In 2023, Reliance Retail, the largest retail chain in India, will start accepting digital rupee payments at its test locations. In March, India began testing an offline function for its CBDC.

Key Players:

Bank Of England

People's Bank of China (PBOC)

European Central Bank (ECB)

Federal Reserve (United States)

Swiss National Bank (SNB)

Bank of Japan (BOJ)

Bank of Canada

Reserve Bank of Australia (RBA)

National Bank of Poland

Reserve Bank of India (RBI)

Several nations intend to introduce Central Bank Digital Currency (CBDC), however, none of them have formally adopted it as of yet. To determine whether CBDC programs are credible, they have all started the first test program and research studies. One of the earliest nations to put forth this notion was England. Not long after, China joined. Russia is about to produce a "crypto Rubel" of its own.

To Learn more about this report,

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. Central Bank Digital Currency (CBDC) Market – Scope & Methodology

1.1 Market Segmentation

1.2 Scope, Assumptions & Limitations

1.3 Research Methodology

1.4 Primary Sources

1.5 Secondary Sources Chapter 2. Central Bank Digital Currency (CBDC) Market – Executive Summary

2.1 Market Size & Forecast – (2024 – 2030) ($M/$Bn)

2.2 Key Trends & Insights

2.2.1 Demand Side

2.2.2 Supply Side

2.3 Attractive Investment Propositions

2.4 COVID-19 Impact Analysis Chapter 3. Central Bank Digital Currency (CBDC) Market – Competition Scenario

3.1 Market Share Analysis & Company Benchmarking

3.2 Competitive Strategy & Development Scenario

3.3 Competitive Pricing Analysis

3.4 Supplier-Distributor Analysis Chapter 4. Central Bank Digital Currency (CBDC) Market - Entry Scenario

4.1 Regulatory Scenario

4.2 Case Studies – Key Start-ups

4.3 Customer Analysis

4.4 PESTLE Analysis

4.5 Porters Five Force Model

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Powers of Customers

4.5.3 Threat of New Entrants

4.5.4 Rivalry among Existing Players

4.5.5 Threat of Substitutes Chapter 5. Central Bank Digital Currency (CBDC) Market – Landscape

5.1 Value Chain Analysis – Key Stakeholders Impact Analysis

5.2 Market Drivers

5.3 Market Restraints/Challenges

5.4 Market Opportunities Chapter 6. Central Bank Digital Currency (CBDC) Market – By Type

6.1 Introduction/Key Findings

6.2 Wholesale CBDC

6.3 Retail CBDC

6.4 Y-O-Y Growth trend Analysis By Type

6.5 Absolute $ Opportunity Analysis By Type, 2024-2030 Chapter 7. Central Bank Digital Currency (CBDC) Market – By Issuance

7.1 Introduction/Key Findings

7.2 Direct CBDC

7.3 Indirect CBDC

7.4 Hybrid CBDC

7.5 Y-O-Y Growth trend Analysis By Issuance

7.6 Absolute $ Opportunity Analysis By Issuance, 2024-2030 Chapter 8. Central Bank Digital Currency (CBDC) Market – By Structure

8.1 Introduction/Key Findings

8.2 Account-based

8.3 Token-based

8.4 Y-O-Y Growth trend Analysis By Structure

8.5 Absolute $ Opportunity Analysis By Structure, 2024-2030 Chapter 9. Central Bank Digital Currency (CBDC) Market , By Geography – Market Size, Forecast, Trends & Insights

9.1 North America

9.1.1 By Country

9.1.1.1 U.S.A.

9.1.1.2 Canada

9.1.1.3 Mexico

9.1.2 By Issuance

9.1.3 By Structure

9.1.4 By Type

9.1.5 Countries & Segments - Market Attractiveness Analysis

9.2 Europe

9.2.1 By Country

9.2.1.1 U.K

9.2.1.2 Germany

9.2.1.3 France

9.2.1.4 Italy

9.2.1.5 Spain

9.2.1.6 Rest of Europe

9.2.2 By Issuance

9.2.3 By Structure

9.2.4 By Type

9.2.5 Countries & Segments - Market Attractiveness Analysis

9.3 Asia Pacific

9.3.1 By Country

9.3.1.1 China

9.3.1.2 Japan

9.3.1.3 South Korea

9.3.1.4 India

9.3.1.5 Australia & New Zealand

9.3.1.6 Rest of Asia-Pacific

9.3.2 By Issuance

9.3.3 By Structure

9.3.4 By Type

9.3.5 Countries & Segments - Market Attractiveness Analysis

9.4 South America

9.4.1 By Country

9.4.1.1 Brazil

9.4.1.2 Argentina

9.4.1.3 Colombia

9.4.1.4 Chile

9.4.1.5 Rest of South America

9.4.2 By Issuance

9.4.3 By Structure

9.4.4 By Type

9.4.5 Countries & Segments - Market Attractiveness Analysis

9.5 Middle East & Africa

9.5.1 By Country

9.5.1.1 United Arab Emirates (UAE)

9.5.1.2 Saudi Arabia

9.5.1.3 Qatar

9.5.1.4 Israel

9.5.1.5 South Africa

9.5.1.6 Nigeria

9.5.1.7 Kenya

9.5.1.8 Egypt

9.5.1.9 Rest of MEA

9.5.2 By Issuance

9.5.3 By Structure

9.5.4 By Type

9.5.5 Countries & Segments - Market Attractiveness Analysis Chapter 10. Central Bank Digital Currency (CBDC) Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments)

Report Code: VMR-203 | Published Date: July 2025 | Format: Excel and PDF

The 3D Scanning Market was valued at USD 2.28 billion in 2024 and is projected to reach a market size of USD 5.37 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CA...

Report Code: VMR-14818 | Published Date: July 2024 | Format: Excel and PDF

The Global Passwordless Authentication Market is expected to grow from USD 22.70 billion in 2025 to approximately USD 49.13 billion by 2030, at a 16.7% CAGR from 2026-2030.

Report Code: VMR-435 | Published Date: March 2024 | Format: Excel and PDF

The Equity Management Software Market was valued at USD 591.85 million in 2023. Over the forecast period of 2024-2030, it is projected to reach USD 1508.47 million by 2030, growing at a CAGR of 14.3%.

Report Code: VMR-15816 | Published Date: March 2024 | Format: Excel and PDF

The global intellectual property (IP) services market was valued at USD 2.8 billion and is projected to reach a market size of USD 6.38 billion by the end of 2030. Over the forecast period of 2024–2030, the market is pro...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”