Building Materials Market Research Report – Segmented By Type (Aggregates, Bricks, Cement, Others); By Application (Residential, Commercial, Industrial); and Region - Size, Share, Growth Analysis | Forecast (2025 – 2030)

Building Materials Market Size (2025 – 2030)

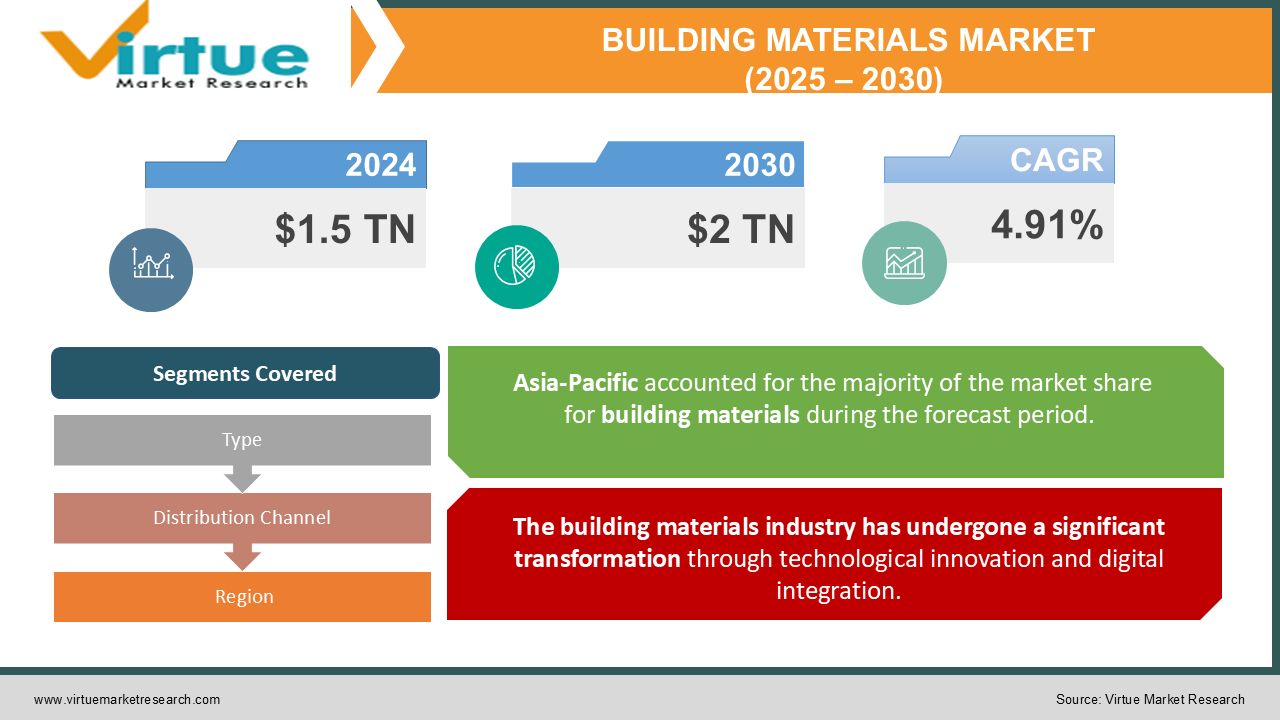

The Building Materials Market was valued at USD 1.5 trillion and is projected to reach a Market size of USD 2 trillion by the end of 2030. Over the forecast period of 2025-2030, the Market is projected to grow at a CAGR of 4.91%.

The building materials market has demonstrated remarkable resilience and growth in 2023, driven by rapid urbanization, infrastructure development, and increasing focus on sustainable construction practices. The industry encompasses a wide range of products from traditional materials like cement, steel, and timber to innovative sustainable alternatives and smart building components. The sector has witnessed significant technological advancements, particularly in developing eco-friendly materials and improving manufacturing processes to reduce environmental impact. The market has shown strong recovery post-pandemic, with increased construction activities across residential, commercial, and industrial sectors. Sustainable building materials have gained particular traction, reflecting growing environmental consciousness among consumers and stricter regulatory requirements for green building practices. The industry has also seen increased adoption of prefabricated and modular construction materials, responding to demands for faster construction timelines and cost efficiency.

Key Market Insights:

Concrete remained the most widely used construction material, with over 30 billion tons used worldwide in 2023.

Green building materials accounted for around 20% of the total market demand in 2023.

Recycled building materials saw a 15% increase in usage, driven by sustainability efforts.

Prefabricated materials contributed $150 billion to the building materials market in 2023.

The demand for structural steel surpassed 1.7 billion tons in 2023 due to urbanization projects.

Wood-based building materials saw a 10% rise in demand, totaling over 500 million cubic meters in 2023.

Concrete block production alone was valued at $75 billion in 2023.

Approximately 5% of the building materials market revenue came from sustainable insulation products.

Ready-mix concrete accounted for over 60% of all concrete used in construction projects in 2023.

Over 500 million square meters of roofing materials were sold globally in 2023.

Building Materials Market Drivers:

The building materials industry has undergone a significant transformation through technological innovation and digital integration.

Advanced manufacturing processes, including artificial intelligence and automation, have revolutionized production efficiency and quality control. Smart sensors and IoT integration enable real-time monitoring of material performance and durability, leading to improved product development and customer satisfaction. Digital twin technology has become instrumental in testing and optimizing building materials before physical production, reducing waste and improving cost-effectiveness. The integration of nanotechnology has led to the development of superior materials with enhanced properties such as self-cleaning surfaces, improved strength-to-weight ratios, and better thermal insulation capabilities. Manufacturers have adopted digital platforms for inventory management, supply chain optimization, and customer relationship management, resulting in streamlined operations and reduced operational costs. The implementation of blockchain technology has improved transparency in material sourcing and supply chain management, addressing concerns about sustainability and ethical procurement.

Environmental consciousness and stringent regulations have emerged as powerful drivers in the building materials market.

Manufacturers are increasingly focusing on developing eco-friendly materials and implementing sustainable production processes in response to growing environmental concerns and regulatory requirements. The industry has witnessed a significant shift toward circular economy principles, with increased emphasis on recycling and reusing materials. Companies are investing in research and development to create innovative materials with lower carbon footprints and reduced environmental impact. The adoption of renewable energy sources in manufacturing processes and the development of carbon-neutral production facilities demonstrate the industry's commitment to sustainability. Government regulations and green building certifications have created a strong market pull for sustainable building materials. Tax incentives and environmental credits have encouraged manufacturers to invest in cleaner technologies and sustainable practices. The growing awareness among consumers about environmental issues has created a premium market for eco-friendly building materials, driving innovation and competition in this sector.

Building Materials Market Restraints and Challenges:

The building materials market faces several significant challenges that impact its growth and development. Raw material price volatility remains a primary concern, with fluctuating costs of essential materials like steel, cement, and timber affecting profit margins and pricing stability. Supply chain disruptions, exacerbated by global events and geopolitical tensions, have created uncertainty in material availability and delivery timelines. Labor shortages in manufacturing and skilled workforce gaps present ongoing challenges for the industry. The technical expertise required for producing advanced building materials and operating sophisticated manufacturing equipment often exceeds available talent pools. Additionally, the high capital investment required for upgrading manufacturing facilities and implementing new technologies creates barriers for smaller players and market entrants. Regulatory compliance costs and environmental standards pose significant challenges, particularly for traditional materials manufacturers transitioning to sustainable practices. The industry also faces challenges in standardization and quality control across different regions and markets. The cyclical nature of the construction industry creates demand uncertainties, affecting production planning and inventory management. Market fragmentation and intense competition have led to price pressures and reduced profit margins. The need to constantly innovate while maintaining cost competitiveness stretches research and development budgets. Additionally, the industry faces challenges in managing waste reduction and implementing effective recycling programs while maintaining product quality and performance standards.

Building Materials Market Opportunities:

The building materials market presents numerous opportunities for growth and innovation. The increasing demand for sustainable and eco-friendly materials opens new markets for innovative products and solutions. The growing trend toward smart buildings and intelligent construction materials creates opportunities for developing integrated building solutions with embedded technology. Emerging markets and rapid urbanization in developing countries offer significant growth potential for building materials manufacturers. The rise of modular and prefabricated construction methods creates opportunities for specialized material development and manufacturing processes. Digital transformation in the construction industry presents opportunities for developing materials with enhanced connectivity and monitoring capabilities. The focus on energy efficiency and green building certifications creates markets for high-performance insulation materials and energy-saving building components. The growing renovation and retrofitting market offers opportunities for specialized materials designed for upgrading existing structures. Additionally, the increasing adoption of 3D printing in construction creates opportunities for developing specialized printing materials and composites. Research in biomimetic materials and nature-inspired solutions offers the potential for developing innovative building materials with superior properties. The trend toward localization of production presents opportunities for establishing regional manufacturing facilities and developing market-specific products. The growing emphasis on disaster-resistant construction creates markets for specialized materials with enhanced durability and resistance properties.

BUILDING MATERIALS MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2024 - 2030

Base Year

2024

Forecast Period

2025 - 2030

CAGR

4%

Segments Covered

By Type, Application and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Key Companies Profiled

CRH plc., Martin Marietta Materials, Inc., Vulcan Materials Company, Heidelberg Materials AG, Anhui Conch Cement Company Ltd., James Hardie Industries plc., CEMEX, S.A.B. de C.V., Taiwan Cement Corp., Eagle Materials Inc., Buzzi Unicem S.p.A.

Building Materials Market Segmentation: By Type

Aggregates

Bricks

Cement

Others

Concrete and cement continue to dominate the market due to their versatility, durability, and cost-effectiveness. The segment accounts for approximately 35% of the total market share.

Composite materials are experiencing the highest growth rate due to their superior properties, including strength-to-weight ratio, durability, and customization possibilities.

Building Materials Market Segmentation: By Application

Residential

Commercial

Industrial

Distributors remain the primary channel, accounting for 40% of sales due to their established networks and ability to handle bulk orders.

E-commerce platforms are showing the highest growth rate, driven by digital transformation and changing customer preferences.

Building Materials Market Segmentation: Regional Analysis

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

Asia-Pacific emerges as both the dominant and fastest-growing region, driven by rapid urbanization, infrastructure development, and economic growth in countries like China and India. The region's dominance is attributed to massive construction projects, government investments in infrastructure, and growing urbanization rates. Strong manufacturing capabilities, cost-competitive production, and increasing domestic demand contribute to its market leadership.

The region's construction boom, particularly in residential and commercial sectors, fuels demand for various building materials. Local manufacturing capabilities, technological advancement, and strategic government initiatives support market growth. The presence of large-scale infrastructure projects, including smart cities and transportation networks, creates sustained demand for building materials

COVID-19 Impact Analysis on the Building Materials Market :

The COVID-19 pandemic significantly impacted the building materials market, causing initial disruptions in supply chains and manufacturing operations. Production facilities faced temporary shutdowns, reduced workforce capacity, and logistics challenges during the early stages of the pandemic. However, the sector demonstrated remarkable resilience and adaptation to the new normal. The pandemic accelerated several trends in the industry, including digitalization of operations and increased focus on sustainable materials. Companies implemented remote monitoring systems and automated processes to maintain operations while ensuring worker safety. The shift toward home improvement projects during lockdowns created unexpected demand in the residential segment. Supply chain disruptions led to increased focus on local sourcing and inventory management strategies. Manufacturers adopted new safety protocols and workplace arrangements, leading to long-term improvements in operational efficiency. The pandemic also highlighted the importance of risk management and supply chain diversification in the industry. Digital transformation initiatives, including e-commerce platforms and virtual customer service, gained momentum during this period. The industry saw increased investment in research and development for antimicrobial materials and touchless solutions. Recovery strategies focused on building resilient supply chains and adopting flexible manufacturing processes.

Latest Trends/ Developments:

The building materials market is experiencing rapid evolution with several emerging trends. Smart building materials with integrated sensors and monitoring capabilities are gaining popularity. These materials can provide real-time data about structural health, environmental conditions, and energy efficiency. Sustainable and bio-based materials are becoming mainstream, with an increased focus on carbon-neutral products. Advanced manufacturing techniques, including 3D printing and automated production, are transforming traditional manufacturing processes. The industry is witnessing the growing adoption of circular economy principles, emphasizing material recycling and waste reduction. Digital transformation continues to reshape the industry through improved supply chain management and customer service. Innovation in nanomaterials and advanced composites is creating new possibilities for high-performance building materials. The trend toward prefabrication and modular construction is driving demand for standardized, pre-engineered materials. Energy-efficient and climate-responsive materials are gaining prominence in response to environmental concerns. The industry is seeing increased integration of renewable energy components in building materials. Developments in self-healing materials and adaptive building components represent cutting-edge innovations in the

Key Players:

CRH plc.

Martin Marietta Materials, Inc.

Vulcan Materials Company

Heidelberg Materials AG

Anhui Conch Cement Company Ltd.

James Hardie Industries plc.

CEMEX, S.A.B. de C.V.

Taiwan Cement Corp.

Eagle Materials Inc.

Buzzi Unicem S.p.A.

To Learn more about this report,

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. Building Materials Market – Scope & Methodology

1.1 Market Segmentation

1.2 Scope, Assumptions & Limitations

1.3 Research Methodology

1.4 Primary Sources

1.5 Secondary Sources Chapter 2. Building Materials Market – Executive Summary

2.1 Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2 Key Trends & Insights

2.2.1 Demand Side

2.2.2 Supply Side

2.3 Attractive Investment Propositions

2.4 COVID-19 Impact Analysis Chapter 3. Building Materials Market – Competition Scenario

3.1 Market Share Analysis & Company Benchmarking

3.2 Competitive Strategy & Development Scenario

3.3 Competitive Pricing Analysis

3.4 Supplier-Distributor Analysis Chapter 4. Building Materials Market - Entry Scenario

4.1 Regulatory Scenario

4.2 Case Studies – Key Start-ups

4.3 Customer Analysis

4.4 PESTLE Analysis

4.5 Porters Five Force Model

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Powers of Customers

4.5.3 Threat of New Entrants

4.5.4 Rivalry among Existing Players

4.5.5 Threat of Substitutes Chapter 5. Building Materials Market – Landscape

5.1 Value Chain Analysis – Key Stakeholders Impact Analysis

5.2 Market Drivers

5.3 Market Restraints/Challenges

5.4 Market Opportunities Chapter 6. Building Materials Market – By Type

6.1 Introduction/Key Findings

6.2 Aggregates

6.3 Bricks

6.4 Cement

6.5 Others

6.6 Y-O-Y Growth trend Analysis By Type

6.7 Absolute $ Opportunity Analysis By Type, 2025-2030 Chapter 7. Building Materials Market – By Application

7.1 Introduction/Key Findings

7.2 Residential

7.3 Commercial

7.4 Industrial

7.5 Y-O-Y Growth trend Analysis By Application

7.6 Absolute $ Opportunity Analysis By Application, 2025-2030 Chapter 8. Building Materials Market , By Geography – Market Size, Forecast, Trends & Insights

8.1 North America

8.1.1 By Country

8.1.1.1 U.S.A.

8.1.1.2 Canada

8.1.1.3 Mexico

8.1.2 By Type

8.1.3 By Distribution Channel

8.1.4 Countries & Segments - Market Attractiveness Analysis

8.2 Europe

8.2.1 By Country

8.2.1.1 U.K

8.2.1.2 Germany

8.2.1.3 France

8.2.1.4 Italy

8.2.1.5 Spain

8.2.1.6 Rest of Europe

8.2.2 By Type

8.2.3 By Distribution Channel

8.2.4 Countries & Segments - Market Attractiveness Analysis

8.3 Asia Pacific

8.3.1 By Country

8.3.1.1 China

8.3.1.2 Japan

8.3.1.3 South Korea

8.3.1.4 India

8.3.1.5 Australia & New Zealand

8.3.1.6 Rest of Asia-Pacific

8.3.2 By Type

8.3.3 By Distribution Channel

8.3.4 Countries & Segments - Market Attractiveness Analysis

8.4 South America

8.4.1 By Country

8.4.1.1 Brazil

8.4.1.2 Argentina

8.4.1.3 Colombia

8.4.1.4 Chile

8.4.1.5 Rest of South America

8.4.2 By Type

8.4.3 By Distribution Channel

8.4.4 Countries & Segments - Market Attractiveness Analysis

8.5 Middle East & Africa

8.5.1 By Country

8.5.1.1 United Arab Emirates (UAE)

8.5.1.2 Saudi Arabia

8.5.1.3 Qatar

8.5.1.4 Israel

8.5.1.5 South Africa

8.5.1.6 Nigeria

8.5.1.7 Kenya

8.5.1.8 Egypt

8.5.1.9 Rest of MEA

8.5.2 By Type

8.5.3 By Distribution Channel

8.5.4 Countries & Segments - Market Attractiveness Analysis Chapter 9. Building Materials Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments)

9.1 CRH plc.

9.2 Martin Marietta Materials, Inc.

9.3 Vulcan Materials Company

9.4 Heidelberg Materials AG

9.5 Anhui Conch Cement Company Ltd.

9.6 James Hardie Industries plc.

9.7 CEMEX, S.A.B. de C.V.

9.8 Taiwan Cement Corp.

9.9 Eagle Materials Inc.

9.10 Buzzi Unicem S.p.A.

Fill out the form below and our team will get back to you shortly

FAQ's

Rapid urbanization and increasing infrastructure projects in both developed and developing regions are propelling the demand for building materials.

The production of traditional building materials, like cement and steel, generates significant carbon emissions, contributing to climate change.

The building materials market is led by several prominent global players who dominate various segments. Lafarge Holcim, Saint-Gobain, HeidelbergCement, CEMEX, and Dow Chemical Company stand out as major contributors to market innovation and growth. Other significant players include CRH plc, Kingspan Group, Owens Corning, BASF SE, and Armstrong World Industries. The market also sees strong competition from companies like Boral Limited, Knauf Gips KG, Guardian Industries, Nippon Sheet Glass Co., and Vulcan Materials Company.

Asia Pacific is the most dominant region in the market, accounting for approximately 35% of the total market share.

Asia Pacific is the fastest-growing region in the market.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-14888 | Published Date: August 2023 | Format: Excel and PDF

Global Paper Pulp Drying System Market was valued at USD 674.29 million and is projected to reach a market size of USD 688.45 million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to...

Report Code: VMR-4071 | Published Date: July 2024 | Format: Excel and PDF

In 2022, the Global Cloud Automation Software for Telecom Industry Market was valued at $3.125 billion, and is projected to reach a market size of $4.72 billion by 2030. Over the forecast period of 2023-2030, market is p...

Report Code: VMR-16121 | Published Date: November 2023 | Format: Excel and PDF

The Dairy Evaporators and Drying Equipment Market was valued at USD 3.24 billion in 2023 and is projected to reach a market size of USD 4.87 billion by the end of 2030. Over the forecast period of 2024-2030, the market i...

Report Code: VMR-17453 | Published Date: September 2024 | Format: Excel and PDF

The Global Robotic Weeding Machines Market was valued at USD 465 million in 2023 and is projected to expand at a compound annual growth rate (CAGR) of 12.8% from 2024 to 2030, reaching USD 1.08 billion by 2030.

Report Code: VMR-4250 | Published Date: September 2024 | Format: Excel and PDF

The global Rare Earth Elements (REE) Market was valued at approximately USD 5.5 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 9% from 2024 to 2030. By 2030, the market is expected to...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”