Animal Vaccines Market Research Report – Segmented by Animal Type (Livestock, Companion Animals, and Aquaculture); by Vaccine Type (Attenuated Live Vaccines, Inactivated Vaccines, Subunit Vaccines, and Recombinant Vaccines); by Mode of Administration (Subcutaneous, Intramuscular, and Intranasal) and Region - Size, Share, Growth Analysis | Forecast (2024 – 2030)

Animal Vaccines Market Size (2024 – 2030)

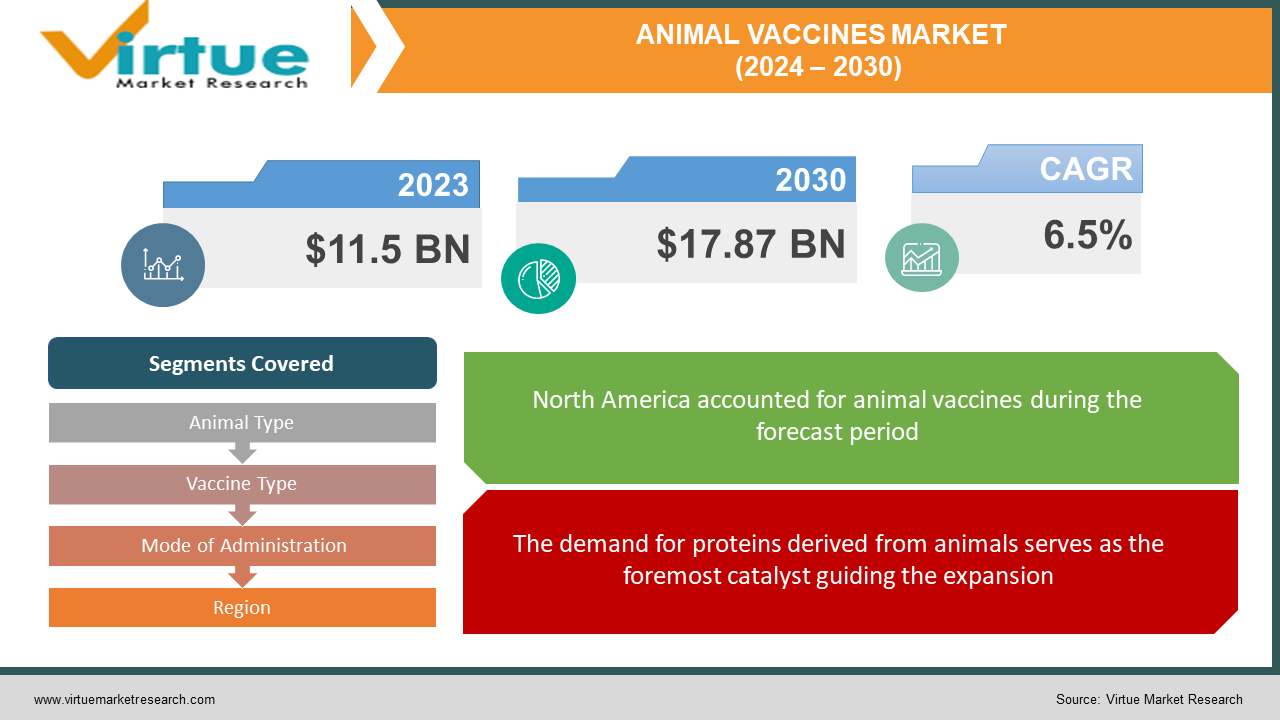

The animal vaccine market was valued at USD 11.5 billion in 2023 and is projected to reach a market size of USD 17.87 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to grow at a CAGR of 6.5%.

The field of animal vaccines has become a cornerstone of modern veterinary medicine and an indispensable tool for safeguarding both animal lives and human health. This dynamic market is shaped by a complex interplay of factors: a relentless need to curb zoonotic disease outbreaks, the demands of global food production, and the heartwarming trend of increased pet ownership. When we think of animal vaccines, it's easy to focus on the benefits for pets, livestock, or farmed fish. While these indeed represent central drivers of the market, the scope of impact extends far beyond animal wellbeing. Zoonotic diseases, transmissible from animals to humans, cause public health crises and economic disruption. Rabies, avian influenza, and the West Nile virus are just a few examples where animal vaccination forms a crucial barrier between harmful pathogens and human populations.

Key Market Insights:

China, India, and Japan are anticipated to exhibit a 7.2% CAGR through 2028 through surging meat production and rising pet adoption.

In the second quarter of 2023, animal healthcare business Zoetis saw a 12% rise in operational adjusted net income and a 9% increase in sales. Strong sales in the companion animal and livestock industries are the reason for this development.

By 2024, the size of the Chinese veterinary vaccine market is expected to reach 450 million yuan.

With a projected total sale of more than eight billion dollars in 2022, American pharmaceutical firm Zoetis is the biggest business in the animal health industry worldwide.

A study by Boston University carried out in 2023 showed that approximately 50% of dog owners are reluctant to vaccinate their animals. To tackle this, organizations have been focusing on educational campaigns to spread awareness. Besides, veterinary outreach has increased, especially in underdeveloped areas.

Animal Vaccine Market Drivers:

The demand for proteins derived from animals serves as the foremost catalyst guiding the expansion.

Of the various key factors propelling the steady expansion of the multi-billion-dollar animal vaccine industry, the most dominant underlying driver stems from the global demand for proteins derived from livestock and aquaculture sources. Per capita, meat consumption has progressively scaled new peaks over recent decades, with global citizens currently consuming over 43 kilograms per year. Several socio-economic undercurrents have guided this unrelenting growth trajectory in meat-eating habits. Rising incomes in heavily populated developing countries have made protein foods more affordable and desirable, with pork and poultry leading demand due to lower prices compared to red meats. The availability of processed and packaged meat products has also enhanced accessibility. At the same time, marketing campaigns by meat exporters and lax sustainability policies have boosted consumption volumes, despite health and ecological caveats. As the world's middle class expands by leaps and bounds, developing nations are particularly witnessing a dramatic shift toward more meat-heavy dietary patterns characteristic of Western lifestyles. The emerging appellation of meat as a status product, especially coveted during cultural celebrations, also continues to propel its soaring popularity within transitioning populations.

Next-generation versions leveraging viral vectors, nucleic acids, and other cutting-edge platforms are steering the industry toward higher-efficacy products.

While traditional modified live or inactivated vaccine platforms have continued to dominate animal vaccine volumes so far due to their known safety and efficacy, various limitations in this decades-old biological technology have left room for improvements in immunization potency. Hence, recent breakthroughs within cutting-edge vaccine engineering spheres are acting as a key driver accelerating the growth of the multi-billion-dollar animal vaccine industry worldwide. Both limitations in the consistency of protection levels as well as logistical bottlenecks have impacted the field efficacy of first-generation vaccine options. The necessity for 2-3 initial doses and annual booster shots with traditional products increases handling stress for livestock and compound production costs for manufacturers. Vaccination campaigns across large commercial flocks also leave immunity gaps due to the practical challenges of assuring administration to every single bird. Furthermore, the demanding cold storage requirements of delicate conventional platforms lead to excessive waste issues in many geographies. Novel vaccine engineering innovations are addressing such limitations to steer the industry toward higher-efficiency next-generation products. Recombinant vector vaccines utilizing viruses like fowl pox as a delivery mechanism to transport target antigens offer a rapid and longer-lasting shield triggered by just a single dose of inoculation. Nucleic acid platforms such as DNA and RNA vaccines can also enable precise stimulation of the immune system guided by specific genes without the need for whole infectious particles. As these can be synthesized chemically, high purity levels aid safety. Alongside enhancing effectiveness, cutting-edge platforms also enable DIVA capability for differentiating infected from vaccinated animals to precisely target control measures during outbreaks.

Animal Vaccine Market Restraints and Challenges:

Assuring smooth supply chains remains a barrier.

While production costs are dropping, non-metallic solutions remain more expensive to manufacture than metals in most cases. Multistep resin and fiber production, the intricacy of combining constituents, and high costs for pre- and post-processing contribute to inflated prices. The convoluted supply chain pathway serving the multi-billion-dollar animal vaccine industry has remained severely fraught with various structural and logistic challenges. From raw material procurement struggles impacting production schedules to gaps in cold chain integrity compromising vaccine viability through the last stretch of transportation, myriad complexities span across the ecosystem. At the manufacturing source, producers consistently grapple with meeting elevated demand for both conventional and next-generation vaccines as protein consumption amplifies livestock populations. Capacity expansion is throttled by bottlenecks in garnering reliable access to essential raw materials like cell culture media and adjuvants, as well as the availability of sterile vials, tanks, and other critical inputs. As nearly 70% of bio-manufacturing infrastructure dwells across the U.S. and Europe, developing regions with the largest farm animal populations face supply deficits. While outsourcing production to contract manufacturers offers temporary relief, quality assurances require oversight. The long, delicate journey traversed by vaccine post-production also suffers from links weakened by inadequate refrigeration and poor logistical coordination. A majority of first-generation inactivated or live-modified animal vaccines retain viability when stored between precise 2–8 °C temperature bands. However, breaching the threshold on either end rapidly degrades sensitive immunizing agents. Staff training gaps and record-keeping additionally complicate the verification of properly administered booster schedules.

Stringent and lengthy regulatory pathways can be challenging to tackle.

Stringent approval frameworks, often spanning years, tend to disadvantage smaller industry players lacking the financial muscle to navigate convoluted review channels. Startups endure high risks of research pipeline derailment if mandated trial protocols overwhelm resources. Researchers highlight glaring gaps in the proportion of vaccine candidates able to progress beyond early development phases compared to the number of candidates attaining eventual commercial launch consent across veterinary medicine. Numerous novel vaccine methodologies targeting improved immunization potency languish in technology incubators and university labs, as the majority of vaccine approvals center on variations of existing platforms rather than novel alternatives. Permitting testing of early vaccine prototypes on limited sample populations under real-life conditions can guide iterative refinement before submitting for comprehensive efficacy and safety reviews essential for full launch consents. Additionally, enhancing structural aspects to bolster regulatory efficiency remains vital to counter the review timeframe lag. Expanding the pool of evaluators can accelerate the assessment of submitted trial data packages for innovator vaccines already subjected to stringent study protocols. Prioritizing applications for technologies targeting protection against economically devastating transboundary diseases also merits consideration to incentivize R&D in impactful but neglected areas like food and mouth disease, or PRRS.

Manufacturers of animal vaccines must strike a careful balance between affordability, profitability, and innovation, coupled with shifting disease outbreaks and market demands.

Animal vaccine manufacturers operate under continuous tension, struggling to align the product affordability interests of high-volume commercial farms and pet owners against profitability pressures from within that allow continued investments in advancing immunization technology. As recurring expenditure necessities rather than one-time treatments within animal health management ecosystems, vaccine doses witness substantial demand elasticity linked to end pricing, especially in developing markets. Statutory price control mechanisms in several countries also restrain the ability to periodically account for fluctuating input costs about raw materials, labor, and transportation that influence delivered pricing. This leaves limited buffer room along margins for manufacturers to channel revenues into R&D for novel platforms as well as expanding manufacturing capacities. Additionally, recurrent waves of animal disease outbreaks like African swine fever or avian influenza trigger spikes in emergency vaccination response efforts financed by state funding, which temporarily deflate market pricing due to a sudden vaccine surplus.

Animal Vaccine Market Opportunities:

The towering growth predictions for the global animal vaccine industry stem largely from optimistic projections around lucrative opportunities dwelling across developing markets in Asia-Pacific, Latin America, and even Africa. Home to nearly 70% of the world's farm animal inventory, these regions exemplify the fastest-expanding protein demand, reflecting rising incomes and urbanization. Development initiatives geared toward upgrading veterinary access down to the farm gate via trained para vets equipped with refrigerator vans that permit directly administered inoculation campaigns rather than dependence on middlemen could hugely uplift rural penetration. Locally active health workers also ensure reliable follow-up booster compliance, which is critical for vaccine effectiveness. Customizing innovation pipelines to serve developing market needs also offers unfulfilled potential.

ANIMAL VACCINES MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2023 - 2030

Base Year

2023

Forecast Period

2024 - 2030

CAGR

6.5%

Segments Covered

By Animal Type, Vaccine Type, Mode of Administration, and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Animal Vaccines Market Segmentation: By Animal Type

Livestock

Poultry (Chickens, Turkeys, etc.)

Cattle (Cows, Buffalo, etc.)

Swine (Pigs).

Sheep and Goats

Companion Animals

Aquaculture

With 60–70% of the market shares overall, the livestock segment—which includes a variety of livestock animals—consistently makes up the largest portion of the animal vaccine market. Due to the vast size of livestock husbandry required to supply the demand for meat, milk, and eggs worldwide, there is a large animal population that needs to be protected and disease-free. Intensive and concentrated farming methods increase the danger of disease transmission, necessitating routine vaccination to prevent significant financial losses. Vaccinating livestock against illnesses like anthrax or brucellosis has a wider effect than only protecting animal populations; it also saves people from contracting zoonotic infections. Companion animals account for 25–35 percent of the market for animal vaccines, making it the sector with the fastest rate of growth. Due to shifting lifestyles and urbanization, people around the world are becoming more and more pet owners as their need for companionship grows. Pets stop being merely animals and start to become part of the family. Pet owners want the greatest possible medical care for their animals, including complete immunizations against serious diseases like canine parvovirus, feline leukemia, and distemper.

Animal Vaccines Market Segmentation: By Vaccine Type

Attenuated Live Vaccines

Inactivated Vaccines

Subunit Vaccines

Recombinant Vaccines

Attenuated live vaccines account for the largest share, around 40% in 2023. It involves the use of live microbes that are weakened to not cause disease but still trigger protective immunity. They offer long-lasting immunity with a single dose and are commonly used for diseases like rabies, rotavirus, cattle plague, etc. Recombinant vaccines are expected to exhibit the fastest growth. It utilizes vector viruses or molecules to deliver target antigens. These vaccines enable rapid and sustained immune responses using the latest biotech approaches. It is gaining traction for pigs, poultry, and companion animals.

Animal Vaccines Market Segmentation: By Mode of Administration

Subcutaneous

Intramuscular

Intranasal

Most animals have subcutaneous injection sites in their necks and behind their shoulder blades. The ability of medications to be injected subcutaneously and absorbed gradually by the body is anticipated to propel market expansion. For animals, the subcutaneous approach also causes less discomfort. Moreover, subcutaneous injection training for veterinary professionals is less complicated. The intranasal segment is the fastest-expanding mode, growing by over 7% annually. It is administered via nasal drops or aerosol sprays that trigger mucosal immunity, preventing pathogen entry through nasal passages, which is important for diseases like kennel cough.

North America has the largest market share. Factors like large populations of livestock and companion animals, strong government support for animal health, and a sophisticated veterinary infrastructure contribute to this dominance. Asia-Pacific is currently considered the fastest-growing region in the animal vaccine market. The expansion of livestock production to meet demands from a growing population in countries like China and India plays a major role. Increased pet ownership and government-sponsored vaccination programs are further pushing the APAC market forward. Europe is another established market. Stringent animal welfare regulations, advanced healthcare systems, and a focus on disease prevention fuel the market in Europe. South America is seeing steady growth. Burgeoning poultry and cattle industries, particularly in Brazil, fuel the demand for animal vaccines. Improving economies and an upsurge in companion animal care add to this market segment. The potential for growth in the Middle East and Africa remains significant. Government focus on food security, the need to curb livestock disease outbreaks, and a gradual increase in companion animal ownership contribute to this positive growth outlook.

COVID-19 Impact Analysis on the Animal Vaccine Market.

The global market for animal vaccinations has been significantly impacted by the COVID-19 outbreak. The supply chain and the manufacture of animal vaccines have been disrupted by lockdowns and travel restrictions. A primary consequence has been the postponement of planned veterinary appointments and animal immunization campaigns. Social distancing standards prevented many pet owners from making unnecessary trips to the vet. There was a decrease in elective operations such as pet vaccines. Regular livestock vaccinations were also impacted, particularly in underdeveloped nations with inadequate access to veterinary care. Due to the gaps in herd immunity caused by this, animal populations are now more susceptible to disease outbreaks. Lockdown-related labor shortages also had an impact on the production of vaccines. A lot of facilities ran into a staffing shortage, which caused production schedules to slow down. Getting consumables and raw materials was also difficult. Delays in shipping compounded the issues. As a result, there was a shortage of some essential vaccinations for companion and production animals. Early in the pandemic, slower animal sales and poorer livestock production also significantly affected the demand for immunizations. But during the latter half of the pandemic, demand began to increase as lockdowns became less frequent. Governments' increasing animal immunization programs and the rise in pet ownership contributed to the market's recovery. Accelerating efforts to create mRNA vaccines for animals that resemble human COVID vaccinations is one of the longer-term effects. Additionally, businesses are concentrating on enhancing vaccination distribution systems and lowering reliance on cold chain logistics. Infrastructure for vaccine production has seen a rise in investment to strengthen supply chain resilience. Growth will be fueled by higher pet healthcare expenditures and a greater emphasis on zoonotic disease prevention. It is anticipated that market revenues will exceed pre-COVID levels due to increased demand and use of next-generation vaccination technology. However, if there are more waves of the pandemic, the consequences of postponing routine animal vaccination regimens and the advent of vaccine shortages in some areas may present difficulties.

Latest Trends/ Developments:

The global animal vaccine market has been experiencing significant growth, fueled by rising pet ownership, increasing consumption of animal proteins, and a greater focus on preventing zoonotic diseases. Novel vaccine platforms: Conventional vaccine production methods are steadily being replaced by innovative technologies like mRNA, DNA, viral vectors, and subunit vaccines. These platforms allow for faster design and development of highly efficacious vaccines compared to traditional approaches. Several animal health majors like Zoetis, Elanco, and Ceva are investing heavily in these platforms to produce vaccines for various bacterial and viral pathogens affecting livestock and companion animals. Needleless vaccine delivery through mucosal routes like nasal, oral, and transdermal is gaining immense traction. Nasal sprays and oral baits eliminate the stress of injection and allow easy administration of booster doses. Transdermal patches are also becoming more popular with pets. Other innovations include microneedle patches and jet injectors that penetrate the skin without traditional hypodermic needles. Companies like ImmuCell and Color Health are bringing novel animal vaccine delivery solutions to market. The use of robotics, interconnected sensors, and advanced analytics allows consistent, high-quality vaccines to be manufactured at scale. Companies like Boehringer-Ingelheim are implementing automation to meet growing demand.

Key Players:

Zoetis

Merck Animal Health

Boehringer Ingelheim

Ceva Santé Animale

Elanco Animal Health

Virbac

Hester Biosciences

Biogénesis Bagó

Phibro Animal Health Corporation

To Learn more about this report,

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. Animal Vaccines Market – Scope & Methodology

1.1 Market Segmentation

1.2 Scope, Assumptions & Limitations

1.3 Research Methodology

1.4 Primary Sources

1.5 Secondary Sources Chapter 2. Animal Vaccines Market – Executive Summary

2.1 Market Size & Forecast – (2024 – 2030) ($M/$Bn)

2.2 Key Trends & Insights

2.2.1 Demand Side

2.2.2 Supply Side

2.3 Attractive Investment Propositions

2.4 COVID-19 Impact Analysis Chapter 3. Animal Vaccines Market – Competition Scenario

3.1 Market Share Analysis & Company Benchmarking

3.2 Competitive Strategy & Development Scenario

3.3 Competitive Pricing Analysis

3.4 Supplier-Distributor Analysis Chapter 4. Animal Vaccines Market Entry Scenario

4.1 Regulatory Scenario

4.2 Case Studies – Key Start-ups

4.3 Customer Analysis

4.4 PESTLE Analysis

4.5 Porters Five Force Model

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Powers of Customers

4.5.3 Threat of New Entrants

4.5.4 Rivalry among Existing Players

4.5.5 Threat of Substitutes Chapter 5. Animal Vaccines Market – Landscape

5.1 Value Chain Analysis – Key Stakeholders Impact Analysis

5.2 Market Drivers

5.3 Market Restraints/Challenges

5.4 Market Opportunities Chapter 6. Animal Vaccines Market – By Animal Type

6.1 Introduction/Key Findings

6.2 Livestock

6.3 Poultry (Chickens, Turkeys, etc.)

6.4 Cattle (Cows, Buffalo, etc.)

6.5 Swine (Pigs).

6.6 Sheep and Goats

6.7 Companion Animals

6.8 Aquaculture

6.9 Y-O-Y Growth trend Analysis By Animal Type

6.10 Absolute $ Opportunity Analysis By Animal Type, 2024-2030 Chapter 7. Animal Vaccines Market – By Vaccine Type

7.1 Introduction/Key Findings

7.2 Attenuated Live Vaccines

7.3 Inactivated Vaccines

7.4 Subunit Vaccines

7.5 Recombinant Vaccines

7.6 Y-O-Y Growth trend Analysis By Vaccine Type

7.7 Absolute $ Opportunity Analysis By Vaccine Type, 2024-2030 Chapter 8. Animal Vaccines Market – By Mode of Administration

8.1 Introduction/Key Findings

8.2 Subcutaneous

8.3 Intramuscular

8.4 Intranasal

8.5 Y-O-Y Growth trend Analysis By Mode of Administration

8.6 Absolute $ Opportunity Analysis By Product Type, 2024-2030 Chapter 9. Animal Vaccines Market , By Geography – Market Size, Forecast, Trends & Insights

9.1 North America

9.1.1 By Country

9.1.1.1 U.S.A.

9.1.1.2 Canada

9.1.1.3 Mexico

9.1.2 By Animal Type

9.1.3 By Vaccine Type

9.1.4 By Mode of Administration

9.1.5 Countries & Segments - Market Attractiveness Analysis

9.2 Europe

9.2.1 By Country

9.2.1.1 U.K

9.2.1.2 Germany

9.2.1.3 France

9.2.1.4 Italy

9.2.1.5 Spain

9.2.1.6 Rest of Europe

9.2.2 By Animal Type

9.2.3 By Vaccine Type

9.2.4 By Mode of Administration

9.2.5 Countries & Segments - Market Attractiveness Analysis

9.3 Asia Pacific

9.3.1 By Country

9.3.1.1 China

9.3.1.2 Japan

9.3.1.3 South Korea

9.3.1.4 India

9.3.1.5 Australia & New Zealand

9.3.1.6 Rest of Asia-Pacific

9.3.2 By Animal Type

9.3.3 By Vaccine Type

9.3.4 By Mode of Administration

9.3.5 Countries & Segments - Market Attractiveness Analysis

9.4 South America

9.4.1 By Country

9.4.1.1 Brazil

9.4.1.2 Argentina

9.4.1.3 Colombia

9.4.1.4 Chile

9.4.1.5 Rest of South America

9.4.2 By Animal Type

9.4.3 By Vaccine Type

9.4.4 By Mode of Administration

9.4.5 Countries & Segments - Market Attractiveness Analysis

9.5 Middle East & Africa

9.5.1 By Country

9.5.1.1 United Arab Emirates (UAE)

9.5.1.2 Saudi Arabia

9.5.1.3 Qatar

9.5.1.4 Israel

9.5.1.5 South Africa

9.5.1.6 Nigeria

9.5.1.7 Kenya

9.5.1.8 Egypt

9.5.1.9 Rest of MEA

9.5.2 By Animal Type

9.5.3 By Vaccine Type

9.5.4 By Mode of Administration

9.5.5 Countries & Segments - Market Attractiveness Analysis Chapter 10. Animal Vaccines Market – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments)

10.1 Zoetis

10.2 Merck Animal Health

10.3 Boehringer Ingelheim

10.4 Ceva Santé Animale

10.5 Elanco Animal Health

10.6 Virbac

10.7 Hester Biosciences

10.8 Biogénesis Bagó

10.9 Phibro Animal Health Corporation

Fill out the form below and our team will get back to you shortly

FAQ's

The demand for proteins derived from animals and next-generation versions leveraging viral vectors, nucleic acids, and other cutting-edge platforms are the main market drivers.

Ensuring a smooth supply chain, stringent and lengthy regulatory pathways, and striking a balance between affordability, profitability, and innovations coupled with shifting disease outbreaks and market demands are the main concerns.

Zoetis, Merck Animal Health, Boehringer Ingelheim, Ceva Santé Animale, Elanco Animal Health, Virbac, Hester Biosciences, Biogénesis Bagó, and Phibro Animal Health Corporation are the major players.

North America currently holds the largest market share.

Asia-Pacific exhibits the fastest growth.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-18737 | Published Date: October 2025 | Format: Excel and PDF

The Radiation Therapy-based Glioblastoma Multiforme Treatment Market was valued at USD 3.72 billion in 2024 and is projected to reach a market size of USD 6.13 billion by the end of 2030. Over the forecast period of 2025...

Report Code: VMR-15695 | Published Date: August 2022 | Format: Excel and PDF

The Placental Stem Cell Therapy for Neurological Disorders Market was valued at USD 464.96 Million and is projected to reach a market size of USD 1,806.95 Million by the end of 2030. Over the forecast period of 2024-2030...

Report Code: VMR-18524 | Published Date: July 2025 | Format: Excel and PDF

The Insurance Market was valued at USD 10.11 trillion in 2024 and is projected to reach a market size of USD 14.65 trillion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a...

Report Code: VMR-7325 | Published Date: July 2025 | Format: Excel and PDF

The Insomnia Market was valued at USD 3.76 billion in 2024 and is projected to reach a market size of USD 4.84 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR...

Report Code: VMR-19021 | Published Date: January 2026 | Format: Excel and PDF

The Oncology Biologics Competitive Benchmarking Market was valued at USD 1.57 billion in 2025 and is projected to reach a market size of USD 2.42 billion by the end of 2030. Over the forecast period of 2026-2030, the mar...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”