Agricultural Tractors Market Research Report – Segmentation By Power Output (Low Power, Mid Power, High Power), By Drive Type (2-Wheel Drive, 4-Wheel Drive), By Application (Plowing and Cultivation, Irrigation),and Region - Size, Share, Growth Analysis | Forecast (2025– 2030)

Agricultural Tractors Market Size (2025 – 2030)

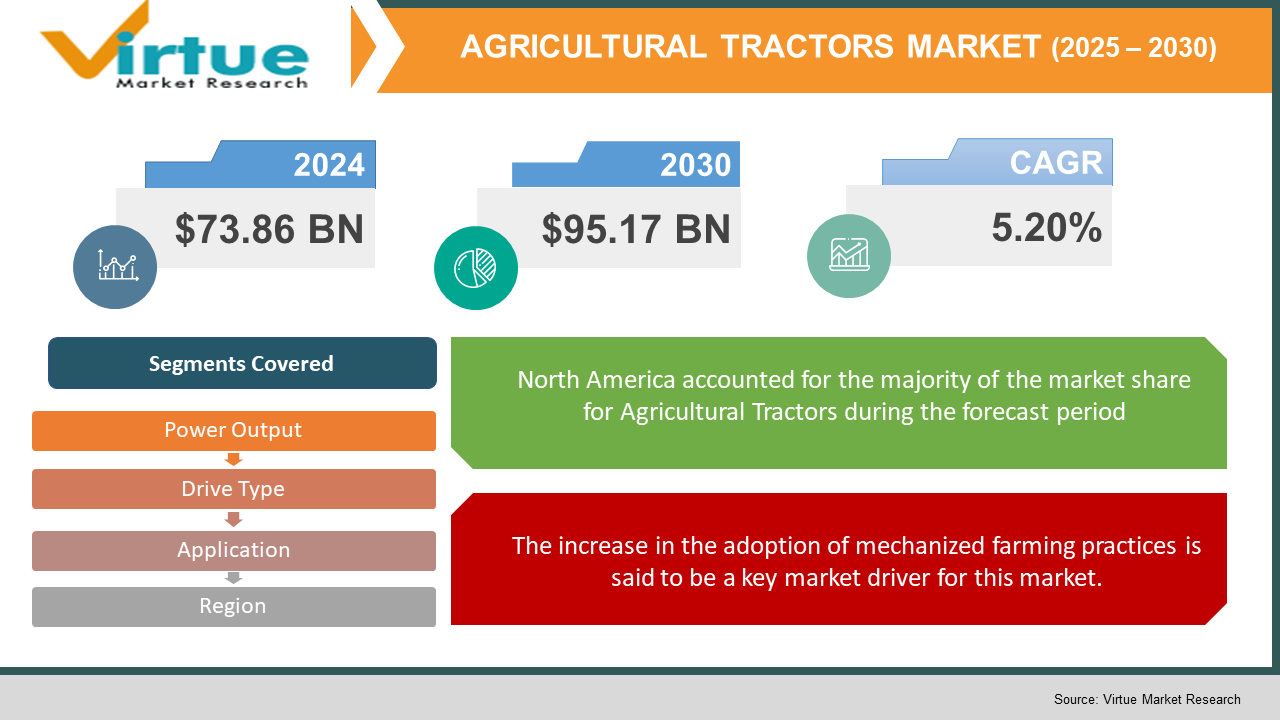

The Global Agricultural Tractors Marketwas valued at USD 73.86 billion and is projected to reach a market size of USD 95.17 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 5.20%.

Rising demand for food caused by a fast-growing global population, technical developments, and increasing mechanization in agriculture all contribute to this growth. Labor shortages in agriculture resulting from rural-to-urban migration have caused farmers to turn to machinery like tractors to keep output rising. These workforce deficiencies and environmental effects will be lessened with the advent of independent technology in agriculture. Still, this transformation carries worries about high first costs and possible job loss.

Key Market Insights:

The use of artificial intelligence (AI) in tractors is improving precision agriculture techniques. For example, artificial intelligence-driven tractors can now map vineyards, analyze data, and assist in intelligent decision-making, hence improving operations and lowering environmental impact.

Five firms control more than 80% of India's tractor market share; Mahindra and Mahindra lead at 42.5%. This concentration suggests a very competitive market, with major obstacles to entry for fresh participants.

Government payments and the need to raise agricultural output are driving fast tractor adoption in the Asia-Pacific region, especially in countries like India and China.

Furthermore, businesses like John Deere are featuring autonomous electric tractors fitted with advanced technology meant to improve output and effectiveness. John Deere introduced a range of autonomous equipment, including battery-electric mowers meant to alleviate labor shortages and lower environmental impact, at the CES 2025 trade event.

Agricultural Tractors Market Drivers:

The increase in the adoption of mechanized farming practices is said to be a key market driver for this market.

To help meet the rising food demand and improve output, farmers all over are increasingly embracing mechanical farming methods. Mechanization speeds up agricultural processes, lowers labor reliance, and improves efficiency. Significantly, economist Hans Binswanger-Mkhize's examination of induced innovation points to the idea that changes in relative factor prices frequently drive technical advances in farming, hence causing improved mechanization.

Rapid innovation in the technical field is considered an important market driver helping the market to grow.

Advanced agricultural tools such as GPS-enabled tractors and autonomous farming equipment are drawing farmers to purchase modern devices. These tools enhance accuracy, effectiveness, and cost-effective labor. For example, precision agriculture methods reduce input dependencies and increase outputs. Studies have shown that significant yield increases are connected with guidance systems, therefore emphasizing the need to introduce them.

Initiatives taken up by governments are a very important market driver.

To encourage modern farming methods, many governments are providing farmers with grants and financial help to buy agricultural equipment, including tractors. Policy reforms, though, could influence these plans. A halt on U. S. federal loans and grants, for instance. Highlighting the sensitivity of the market to government policies inflicted financial disturbances for countryside companies that had invested in machinery based on guaranteed rebates.

Agricultural Tractors Market Restraints and Challenges:

The high levels of initial investment are a great challenge that is faced by the market.

Buying new farm tractors calls for serious funds, which might be a major impediment, especially for small-scale farmers. Modern tractors fitted with sophisticated technology are now more expensive, therefore challenging low-income farmers to buy such machinery. Prolonged use of obsolete equipment caused by this financial obstacle can slow down farming activities and lower output and efficiency.

Modern tractors demand high maintenance costs, acting as a huge market restraint.

Ongoing maintenance and operating costs characterize modern tractors, particularly those linked to advanced technologies. The intricacy of these devices sometimes calls for specialized maintenance work, hence increasing maintenance expenses. Furthermore, under discussion is "right-to-repair," which is gaining visibility as companies like John Deere are criticized for limiting access to repair information, hence forcing farmers to trust authorized service centers, which may be more costly. For example, John Deere has been charged with leaving right-to-repair language out of their manuals, therefore impeding farmers from doing self-repair.

The use of diesel-based tractors raises concerns regarding the environment, hence acting as a great market challenge.

Diesel-powered tractors produce nitrogen oxides and particulate matter, among other pollutants, therefore adding to global warming and environmental degradation. Regulatory agencies have reacted by setting tighter emissions criteria to lessen these effects. For instance, the 2008 Statewide Truck and Bus Rule from the California Air Resources Board (CARB) mandated that heavy-duty diesel trucks retrofit or replace engines to lower emissions. Almost all relevant automobiles must, by January 1, 2023, have engines comparable to those of the 2010 model year, as directed by this rule. For farmers, following these rules can be expensive, so they must invest in updated, less pollutant machinery or retrofit already installed machinery.

The frequent fluctuations in the prices of the commodity are considered a major market challenge.

Fluctuations in commodity prices, driven by variables such as trade policies, worldwide market demand, and weather conditions, may have a profound impact on the agricultural industry. Significant changes in prices could seriously affect the income of farmers and, therefore, their capacity to purchase new equipment, such as tractors. Low commodity prices sometimes cause farmers to postpone or abandon buying new equipment, therefore reducing demand in the agricultural machinery sector. On the other side, high goods prices might justify investment but might also result in higher tool expenses because of growing demand.

Agricultural Tractors Market Opportunities:

The development of electric tractors presents an opportunity for the market to expand as it reduces emission and operational costs.

Electric tractors offer great chances to cut emissions and operational expenditures, therefore supporting worldwide goals of sustainability, so their introduction and growth are in line with this. Companies that produce tractors are instead actively investing in alternative energy sources. New Holland Agriculture, for example, has created the NH2 hydrogen-powered tractor, which offers a sustainable alternative to conventional diesel-powered equipment by releasing just heat, vapor, and water. This development is one of their Energy Independent Farm project meant to help farmers produce their energy from clean sources.

The establishment of rental services has helped small-scale farmers to afford these modern trucks, thereby helping the market to grow.

Starting tractor rental businesses can help small farmers contingent on expanding market size who cannot buy new machinery. Sharing equipment is becoming easier on digital platforms, therefore maximizing machinery usage. Agriculture equipment-sharing platforms like Hello Tractor and WeFarmUp let farmers rent hardware as necessary, therefore lessening the financial weight of purchase. This approach encourages the prudent use of resources within the farming industry as well as raises access to sophisticated technology.

The services provided post sales is another market opportunity that can help the market to grow.

Offering spare parts, maintenance, and repair support may strengthen consumer loyalty and help to generate more income. The need for expert maintenance and repair solutions is growing in line with the technological advancement of agricultural equipment. By providing thorough aftermarket support, companies guarantee equipment longevity and excellent performance for their consumers and, thus, set themselves apart in the marketplace. This strategy not only builds trust but also stimulates repeat trade and great word-of-mouth references.

Expansion into the developing regions can be a good opportunity for the market to increase its reach.

Growing into developing nations with significant agriculture provides great growth possibilities, especially where mechanization is yet to be mature. Often, these areas show an increasing need for contemporary farming techniques to enhance output and satisfy food security requirements. Affordable and flexible tractor solutions introduced by businesses will enable them to explore these markets, thus driving agricultural growth and building a robust market presence. Successful market entry and acceptance depend on partnerships with local actors and knowledge of local agriculture practices.

AGRICULTURAL TRACTORS MARKET REPORT COVERAGE:

REPORT METRIC

DETAILS

Market Size Available

2024 - 2030

Base Year

2024

Forecast Period

2025 - 2030

CAGR

5.20%

Segments Covered

By poer output, application, drive type, and Region

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regional Scope

North America, Europe, APAC, Latin America, Middle East & Africa

Agricultural Tractors Market Segmentation: By Power Output

Low Power

Mid Power

High Power

The mid-power segment is the dominant one, and the high-power segment is the fastest-growing one. Middle Power (40-100 HP) tractors command the market owing to their adaptability and fit for a broad spectrum of farming operations. Usually employed for small-scale farming, gardening, and light work, these tractors have less than 40 horsepower. They have regional popularity in places with divided land holdings. Driven by farm consolidation and the need for effective large-scale operations, high-power (above 100 HP) tractors are the fastest-growing segment. Ideal for medium to large farming enterprises, these tractors, ranging from 40 to 100 horsepower, handle planting, harrowing, and plowing, among other chores. Their acceptance is quite general, and their usefulness is great.

Intended for large-scale commercial agriculture, high-power tractors are used for heavy applications, including deep plowing and large-scale harvesting. This tilling is done by tractors.

Agricultural Tractors Market Segmentation: By Drive Type

2-Wheel Drive

4-Wheel Drive

The 2-Wheel Drive is the dominant segment of the market, and the 4-Wheel Drive is the fastest-growing segment. Presently, two-wheel drive (2WD) tractors dominate the scene since they are cost-effective and suitable for many farming conditions. Their market share is provided by this. Generally, two-wheel-drive tractors are more economical and appropriate for dry and less challenging terrain. Generally, they find application in areas having level topography. Particularly in areas needing more power and flexibility, four-wheel drive (4WD) tractors are the fastest growing. Ideal for demanding terrain and heavy-duty work, four-wheel drive (4WD) tractors provide superior traction and power. Preferred in regions with hilly topography or strong soil qualities.

Agricultural Tractors Market Segmentation: By Application

Plowing and Cultivation

Irrigation

The plowing and Cultivation segment is considered the dominant one, whereas the irrigation segment is the fastest-growing segment. Two basic agricultural methods required to prepare soil and control weeds are plowing and cultivation. These activities make this sector prevalent in the market as tractors fitted with tools such as plows and harrows are widely used. Mechanization's broad acceptance in agriculture has resulted in more need for tractors in plowing and cultivation operations. Increasing demand for effective water management in agriculture is driving rapid expansion of the irrigation industry. By driving pumps, carrying water, and running irrigation machinery, tractors are essential for irrigation. Further driving the need for specialized tractors has been the acceptance of modern irrigation methods like drip and sprinkler systems. The rising popularity of the use of tractors in irrigation systems that helps growers to best use water and increase crop yields has driven the sector's fast growth.

Agricultural Tractors Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

North America is leading in this market, followed by Europe and the Asia-Pacific region. Whereas the South America and MEA regions are considered emerging markets. Large-scale agriculture and extensive use of sophisticated equipment define North America. Nations like India and China are rapidly developing as a result of their agricultural mechanization projects. Africa is experiencing fast development from growing investments in agricultural mechanization intended to improve productivity.

COVID-19 Impact Analysis on the Global Agricultural Tractors Market:

The coronavirus outbreak had a big influence on the market for agricultural tractors, which resulted in long-term industry changes as well as short-term disruptions. The effect depended on a number of elements, including supply chain disturbances, labor scarcity, financial pressures, and changing consumer demand, as well as on location. Mostly obtained from China, India, and Europe, vital tractor components, including engines, transmissions, hydraulics, and electronics, saw distribution disruptions worldwide due to the epidemic. Lockdown measures resulted in limited staff availability and brief factory closures. Delays in manufacturing schedules affected businesses like CNH Industrial, John Deere, and Kubota. Limitations on travel and commerce left tractors and replacement components hard to ship and distribute, so length times for deliveries were raised. Labor shortages caused by migration policies and social distancing rules affected farming operations. Reduced farm worker numbers in nations like India and the United States raised the need for mechanization, hence somewhat offsetting demand loss. Rising understanding of the value of automation, precision farming, and sustainable agriculture by governments and private investors resulted in renewed interest in high-tech tractors, GPS-enabled gear, and electric models. The pandemic sped up developments toward electrification, smart tractors, and automation, therefore positioning the business for long-term technological evolution.

Latest Trends/ Developments:

Seeking to lower labor dependency and improve accuracy in farming activities, the advancement of autonomous tractors is gaining velocity.

Telematics in tractors enable real-time monitoring and data analysis, therefore enhancing maintenance planning and efficiency by means of rebalance.

To lower carbon footprints in agriculture, an increasing number of people are turning to greener tractors, including electric and hybrid varieties.

Key Players:

John Deere

CNH Industrial

Kubota Corporation

AGCO Corporation

Mahindra & Mahindra Ltd.

Class KGaA mbH

SDF Group

Yanmar Co., Ltd.

Escorts Limited

Massey Ferguson

To Learn more about this report,

Global automotive lighting refers to all vehicle lighting systems, from headlamps that illuminate the road to taillights that communicate movements. They guarantee motorists and other road users alike safety, visibility, and style. While taillights frequently use LEDs for improved visibility, headlights are available in a variety of technologies, including LED and laser. Interior illumination, DRLs, and signal lights all have a role to play. This market, which was estimated to be worth $33.64 billion in 2022, is anticipated to rise to $67.39 billion by 2030 because of laws, luxury tastes, safety concerns, and technological developments like OLED taillights and adaptive headlights. Anticipate a future dominated by intelligent, connected, personalized, and sustainable lighting systems that enhance the safety, efficiency, and aesthetic appeal of automobiles.

Key Market Insights:

Car lighting works its magic to provide safety, visibility, and style. Headlights cut through the night, taillights express intent, and interiors shine with comfort. The billion-dollar global business is expected to rise due to consumer demand for high-end experiences, safer roads, and cutting-edge technology. Imagine dynamic messages being painted by taillights, headlights that adjust to the road, and interiors that customize their atmosphere. Driven by technological advancements like linked systems and laser beams, this future is calling. Anticipate even more visually attractive, environmentally friendly, and intelligent lighting to illuminate the way ahead, making cars safer, more efficient, and unquestionably cooler.

Global Automotive Lighting Market Drivers:

Using cutting-edge technology to illuminate the road, safety serves as a guiding light.

In the market for automobile lighting, safety is the driving force behind demand from the public and laws. While automated high beams smoothly react to traffic, adaptive headlights modify their beams so as not to blind other people. With visually striking displays, dynamic taillights convey intentions for braking and turning. Beyond these developments, integrated pedestrian identification and lane departure alerts will soon make roads safer and brighter for everyone.

Beyond Performance-Based Luxuries Redefined by Light.

Luxurious automobile lighting creates a distinct visual identity that goes beyond simple illumination. Personalized interior lighting customizes the driving experience by setting the mood with a range of colours and intensities, while intricate designs and distinctive DRLs modify exteriors. As you approach your automobile at night, welcoming lights lead the way, resulting in an interior that is perfectly lit. Not only is this symphony of light aesthetically pleasing, but it also stands as a tribute to luxury. Upcoming developments like gesture-controlled lighting and holographic displays promise to further enhance the experience.

Fuel Efficiency Takes the Lead: Illuminating Sustainability

The worldwide automotive lighting market is undergoing a significant transition towards energy-efficient solutions, as environmental concerns gain prominence. LED technology is leading the way, providing a ray of hope for the environment and drivers alike. LED lights beam brighter and use a lot less energy than conventional halogen lamps. There are some tangible advantages to this. For drivers, this translates to increased fuel economy, which lowers petrol prices and lessens reliance on fossil fuels. Greater air quality and a reduction in the transport sector's contribution to climate change are the results of reduced overall emissions.

To Learn more about this report,

Global Automotive Lighting Market Restraints and Challenges:

Although the global automotive lighting business is booming, there are still unknowns. Difficulties impede growth even as innovation propels it with eye catching features like laser beams and adaptable headlights. These technologies are luxury items due to their high cost and difficult integration, which puts producers' abilities to the test. The worldwide patchwork created by unclear legislation limits the potential of innovation. Durability issues persist, particularly when complex systems are subjected to challenging conditions. Ultimately, a lot of drivers still don't fully understand how these improvements can help them. Together, we can overcome these obstacles. The keys to reducing costs are improved production, more seamless integration, and unified regulations. Their full potential can be realized by educating customers about the safety, efficiency, and aesthetic value of these lighting wonders. By working together, we can pave the way for an even brighter and safer future for vehicle lighting.

Global Automotive Lighting Market Opportunities:

It is made possible by advanced LED technology, which gives drivers the ability to customize their illumination for the highest level of comfort and flair. Consumers that care about the environment want greener products, and vehicle lighting complies. While solar- and self-powered lighting technologies offer a future powered by clean energy, energy-efficient LEDs lower pollution. The advent of connected lighting systems heralds a new age. Envision automobiles interacting with infrastructure and one another to minimize accidents and enhance traffic efficiency. Integrated headlights with pedestrian recognition provide unmatched safety, while dramatic taillights with eye-catching displays alert onlookers to your intentions. The possibilities are endless in the future. Gesture-controlled interior illumination, holographic displays projected onto the road, and even light fixtures with self-healing capabilities.

AUTOMOTIVE LIGHTING MARKET REPORT COVERAGE:

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Application

Exterior Lighting

Interior Lighting

Due to laws requiring safety features like headlights, taillights, and brake lights, exterior lighting presently holds the most market share in the vehicle lighting industry. The dominance of this market is partly attributed to advancements in safety-focused technologies such as adaptive headlights and daytime running lights. The market value of external lighting is increased by the quick adoption of technology like LED bulbs and laser lights, which improve performance and aesthetics. Conversely, the interior lighting market is expected to increase at the fastest rate in the upcoming years. Innovations like ambient lighting and technology breakthroughs like LED and OLED displays, driven by consumer demand for comfort and personalisation, open new possibilities. The spread of sophisticated interior lighting systems is further driven by the growing emphasis on safety and the expansion of the luxury car market.

Global Automotive Lighting Market Segmentation: By Technology

Halogen

LED (Light-Emitting Diode)

Xenon

Emerging Technologies

The worldwide vehicle lighting market is currently dominated by halogen because of its more affordable price, advanced technology, and useful illumination. With its dependable supply chain and affordable option for manufacturers and cost-conscious customers, halogen holds the biggest market share. The fastest-growing market right now is LEDs, which are predicted to shortly overtake halogen. The rapid expansion of LEDs is driven by their higher efficiency, longer lifespan, flexibility in design, and technological breakthroughs including enhanced brightness. Because LEDs use less energy and produce fewer emissions and better fuel economy, they are becoming more and more popular in the changing automotive lighting market.

Global Automotive Lighting Market Segmentation: By Vehicle Type

Passenger Cars

Commercial Vehicles

Passenger automobiles rule the worldwide automotive lighting market. The sheer number of passenger cars produced which surpasses that of business vehicles and fuels the need for lighting systems is the primary cause of this popularity. The growing demand for personal automobiles in developing nations is a result of rising disposable income, which in turn drives the rise of the passenger car market. The importance that consumers place on safety and aesthetics elements helps to drive market expansion. But in the upcoming years, the market for electric and hybrid cars is expected to develop at the quickest rate. The exponential rise of the worldwide electric car market, which is still expanding and shows no signs of slowing down, is what is driving this surge. Specialised lighting solutions are required since electric and hybrid vehicles have different lighting requirements because of their specific functionality and design aesthetics.

Global Automotive Lighting Market Segmentation: By Sales Channel

OEM (Original Equipment Manufacturers)

Aftermarket

Most lighting systems sold nowadays are sold by OEMs (Original Equipment Manufacturers), primarily because manufacturers pre-install lighting systems in new cars. But in the next years, the aftermarket is expected to develop at the quickest rate. This spike in demand for replacement parts, especially lighting systems, can be linked to several variables, one of them being the average age of cars. The industry is expanding because of consumers' growing desire to personalise their cars with aftermarket lighting upgrades such LED upgrades and decorative lighting. The availability and affordability of technologies like adaptive headlights and laser lights in the aftermarket, together with other advancements in lighting technology, are driving demand even more. Moreover, the growing market for electric cars (EVs).

To Learn more about this report,

Global Automotive Lighting Market Segmentation: By Region

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Throughout the forecast period, Asia Pacific is anticipated to be the automotive lighting market with the highest profitability. Over the past few years, Asia Pacific countries like China and India have seen notable increases in automotive manufacturing and sales, primarily in the medium-to premium luxury car segment. Asia Pacific is predicted to see an increase in the manufacturing of passenger cars, with India experiencing the strongest growth rate. Depending on the state of the national economy, the area offers a suitable selection of both high-end and cheap cars. For instance, there is a substantial demand for halogen, Xenon/HID, and LED since China and India produce more economy and mid-range automobiles. On the other hand, luxury car adoption rates are greater in South Korea and Japan, where LED lighting is the norm.

COVID-19 Impact Analysis on the Global Automotive Lighting Market:

A brief shadow was thrown by COVID-19 over the worldwide automotive lighting market. Production was stopped by lockdowns and supply chain disruptions, while luxury lighting upgrades were shelved by consumers on a tight budget. Resources became scarce, and R&D stagnated. Still, the market is recovering thanks to resurgent demand and rearranged priorities. While energy-efficient LEDs are being pushed towards adoption by sustainability, safety concerns are driving interest in features like pedestrian detection and adaptive headlights. The digital push of the epidemic creates opportunities for intelligent, networked lighting systems that may interact with infrastructure and other cars. Ultimately, the industry is positioned to shine brighter, focused on safety, sustainability, and a connected future, even though the pandemic dimmed its brilliance.

Recent Trends and Developments in the Global Automotive Lighting Market:

A development collaboration between OSRAM Continental and REHAU aims to incorporate lighting into external components, providing automobile manufacturers with innovative lighting options that improve functionality and design flexibility. For rear combination lamps, Hella unveiled a revolutionary lighting innovation called Hella FlatLight technology. A Memorandum of Understanding (MoU) was signed by Samvardhana Motherson Automotive Systems Group BV (SMRPBV), a division of Motherson Group, and Marelli Automotive Lighting to investigate a technology collaboration focused on intelligently lighted external body components. Valeo debuted their revolutionary 360° lighting system at the Shanghai Auto Show. This technology surrounds the car with a band of light, projecting instantaneous, clear signs that other drivers can see from a distance. Pedestrians, cyclists, and scooter riders are especially susceptible to these signals

Key Players:

AMS Osram

Cree

Hella

Hyundai Mobis

Koito

Luminus Devices

Magneti Marelli

Osram Licht AG

Stanley Electric

Valeo

Chapter 1. Agricultural Tractors Market – SCOPE & METHODOLOGY

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources Chapter 2. Agricultural Tractors Market – EXECUTIVE SUMMARY

2.1. Market Size & Forecast – (2025 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.3. Attractive Investment Propositions

2.4. COVID-19 Impact Analysis Chapter 3. Agricultural Tractors Market – COMPETITION SCENARIO

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Drive Type Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis Chapter 4. Agricultural Tractors Market - ENTRY SCENARIO

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.4. PESTLE Analysis

4.5. Porters Five Force Model

4.5.1. Bargaining Power of Suppliers

4.5.2. Bargaining Powers of Customers

4.5.3. Threat of New Entrants

4.5.4. Rivalry among Existing Players

4.5.5. Threat of Substitutes Players

4.5.6. Threat of Substitutes Chapter 5. Agricultural Tractors Market - LANDSCAPE

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities Chapter 6. Agricultural Tractors Market – By Power Output

6.1 Introduction/Key Findings

6.2 Low Power

6.3 Mid Power

6.4 High Power

6.5 Y-O-Y Growth trend Analysis By Power Output

6.6 Absolute $ Opportunity Analysis By Power Output , 2025-2030

Chapter 7. Agricultural Tractors Market – By Drive Type

7.1 Introduction/Key Findings

7.2 2-Wheel Drive

7.3 4-Wheel Drive

7.4 Y-O-Y Growth trend Analysis By Drive Type

7.5 Absolute $ Opportunity Analysis By Drive Type , 2025-2030

Chapter 9. Agricultural Tractors Market, BY GEOGRAPHY – MARKET SIZE, FORECAST, TRENDS & INSIGHTS

9.1. North America

9.1.1. By Country

9.1.1.1. U.S.A.

9.1.1.2. Canada

9.1.1.3. Mexico

9.1.2. By Drive Type

9.1.3. By Application

9.1.4. By Power Output

9.1.5. Countries & Segments - Market Attractiveness Analysis

9.2. Europe

9.2.1. By Country

9.2.1.1. U.K.

9.2.1.2. Germany

9.2.1.3. France

9.2.1.4. Italy

9.2.1.5. Spain

9.2.1.6. Rest of Europe

9.2.2. By Drive Type

9.2.3. By Application

9.2.4. By Power Output

9.2.5. Countries & Segments - Market Attractiveness Analysis

9.3. Asia Pacific

9.3.1. By Country

9.3.1.1. China

9.3.1.2. Japan

9.3.1.3. South Korea

9.3.1.4. India

9.3.1.5. Australia & New Zealand

9.3.1.6. Rest of Asia-Pacific

9.3.2. By Drive Type

9.3.3. By Application

9.3.4. By Power Output

9.3.5. Countries & Segments - Market Attractiveness Analysis

9.4. South America

9.4.1. By Country

9.4.1.1. Brazil

9.4.1.2. Argentina

9.4.1.3. Colombia

9.4.1.4. Chile

9.4.1.5. Rest of South America

9.4.2. By APPLICATION

9.4.3. By Drive Type

9.4.4. By Power Output

9.4.5. Countries & Segments - Market Attractiveness Analysis

9.5. Middle East & Africa

9.5.1. By Country

9.5.1.1. United Arab Emirates (UAE)

9.5.1.2. Saudi Arabia

9.5.1.3. Qatar

9.5.1.4. Israel

9.5.1.5. South Africa

9.5.1.6. Nigeria

9.5.1.7. Kenya

9.5.1.8. Egypt

9.5.1.9. Rest of MEA

9.5.2. By APPLICATION

9.5.3. By Drive Type

9.5.4. By Power Output

9.5.5. Countries & Segments - Market Attractiveness Analysis Chapter 10. Agricultural Tractors Market – Company Profiles – (Overview, Power Output Portfolio, Financials, Strategies & Developments)

10.1 John Deere

10.2 CNH Industrial

10.3 Kubota Corporation

10.4 AGCO Corporation

10.5 Mahindra & Mahindra Ltd.

10.6 Class KGaA mbH

10.7 SDF Group

10.8 Yanmar Co., Ltd.

10.9 Escorts Limited

10.10 Massey Ferguson

Fill out the form below and our team will get back to you shortly

FAQ's

Rising mechanization in agriculture, technical innovations, official subsidies, and the need to improve productivity to satisfy increasing food demand are driving the growth of this market.

Tractor manufacturing and delivery were slowed by the epidemic's disturbance of supply chains and labour availability. Nevertheless, the focus on food security has revitalized interest in agricultural mechanization.

Rising trends are the advancement of autonomous (self-driving) tractors, the incorporation of telematics for real-time monitoring, and the transition to electric and hybrid designs in support of sustainability.

Government campaigns encouraging mechanization should cause the Asia-Pacific area to experience notable development; North America is also growing quickly, thanks to technological advances and big farming operations.

High initial investment costs, operating expenditures, emission-related environmental issues, and variable commodity prices impacting the buying power of farmers are among the difficulties faced by the market.

More related reports

Get expert-driven market research reports from a leading research partner to help you navigate the future of the global industry.

Report Code: VMR-3605 | Published Date: March 2024 | Format: Excel and PDF

The global agricultural harvesting market was valued at USD 23.63 billion and is projected to reach a market size of USD 39.98 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to...

Report Code: VMR-453 | Published Date: December 2024 | Format: Excel and PDF

The Commercial Seaweeds Market was valued at USD 11.54 billion in 2024. Over the forecast period of 2025-2030, it is projected to reach USD 18.11 billion by 2030, growing at a CAGR of 7.8%.

Report Code: VMR-18664 | Published Date: October 2024 | Format: Excel and PDF

The Asia Pacific Farm Mechanization Market was valued at USD 75.2 billion in 2024 and is projected to reach a market size of USD 118.6 billion by the end of 2030.

Report Code: VMR-3441 | Published Date: June 2024 | Format: Excel and PDF

The Agricultural Pesticide Market was valued at USD 48.3 billion in 2023 and is projected to reach a market size of USD 80.13 billion by the end of 2030. Over the cast period of 2024 – 2030, the figure for requests is pr...

Report Code: VMR-17018 | Published Date: May 2024 | Format: Excel and PDF

The Global Metaverse in indoor farming Market is valued at USD 536.55 Million and is projected to reach a market size of USD 761.11 Million by the end of 2030. Over the forecast period of 2024-2030, the market is project...

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”

Medical Devices Company based in Europe

“We received a complex piece of work for our niche market from Virtue Market research in short period of time. I appreciate the quality and content of the final files we received. Thanks for the support”